A Quick Pitch for Semler Scientific and its Bitcoin Strategic Reserve ($SMLR)

A medical technology company trading near the NAV of its Bitcoin reserve and a discounted opeating business.

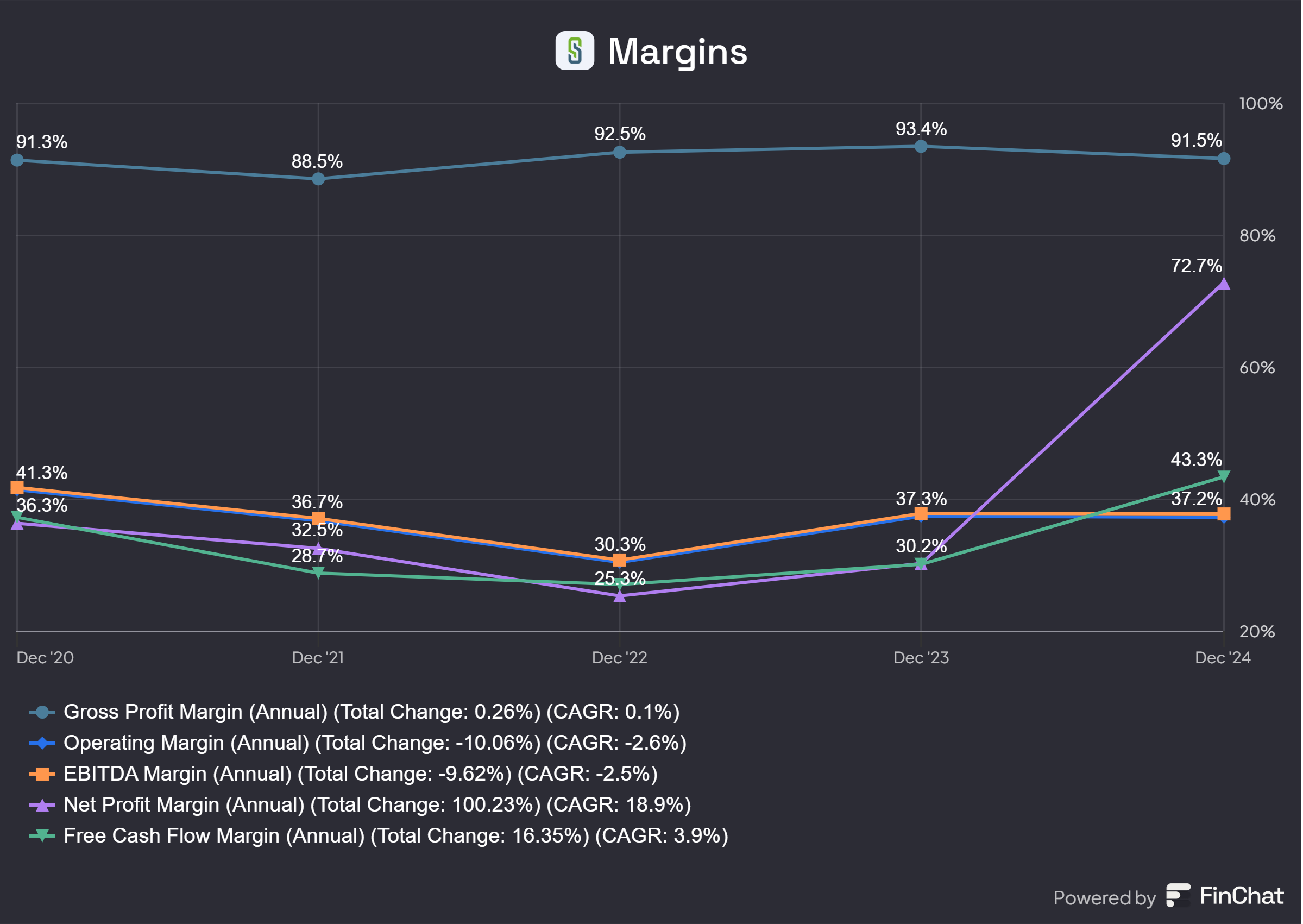

This is a time sensitive idea, so I’m just going to jump right into the overall thesis. It’s actually my second go around because on the first one the price quickly appreciated to around $46 a share before I could publish. The company in focus is Semler Scientific Inc. Semler Scientific is a U.S.-based medical technology company focused on developing products and services that assist in the early detection and management of cardiovascular diseases. Its flagship product is QuantaFlo, a non-invasive, point-of-care test used to diagnose peripheral arterial disease (PAD). Historically, QuantaFlo has been highly cash generative for the company with historical operating margins over 35%, and allowed it to build up substantial cash reserves. In May 2024, Semler’s board of directors approved a shift in treasury strategy, authorizing the use of surplus cash to purchase Bitcoin. This decision marked Semler as the second publicly traded U.S. company to adopt Bitcoin as a primary treasury reserve asset, following Micheal Saylor’s Strategy.

At Semler’s current share price, I believe the company is trading near the net asset value (NAV) of its treasury assets, implying that the market is assigning little to no value to its healthcare operations. This presents a potential disconnect between intrinsic value and market price, offering investors exposure to both an established core business and significant Bitcoin holdings at a slightly discounted valuation. Let’s lay this out in a sum-of-the-parts valuation.

As of Semler’s most recent 10-Q and 8-K filings, the company holds 4,449 Bitcoin. At a current BTC price of approximately $109,500, this equates to a total value of $487.166 million, or $37.07 per share based on the 13.141074 million shares outstanding.

In addition, Semler holds an estimated $76.19 million in cash, cash equivalents, and short-term investments. This figure includes $9.99 million reported in the latest 10-Q, plus $136.2 million in net proceeds from a 3.54 million-share stock offering, offset by $70 million used to acquire additional Bitcoin.

On the liability side, the company faces a $29.75 million legal settlement related to an ongoing DOJ investigation and carries $100 million in convertible bond debt due in 2030.

Adjusting for these items, the net asset value (NAV) is approximately:

$487.166(BTC) + $76.2M (cash) - $29.75M (legal) - $100M (debt) = $433.616M

Divided by 13.14 million shares, this yields an NAV of roughly $33 per share.

With the stock currently trading around $34, the market is effectively valuing the operating business at just $1 per share. This is low given that Semler’s core healthcare segment has generated an average of $17.96 million in free cash flow annually over the past five years, or approximately $1.87 per share using 2024 pre-diluted shares outstanding prior to the share issuance funding their BTC purchase. That implies a P/FCF multiple of just 1.83x.

Admittedly, the core business has faced substantial headwinds recently. However, I expect it to remain viable moving out. Based on a conservative DCF model that assumes $5 million in FCF annually over the next five years at a 12% discount rate, I estimate the standalone value of the operating business at approximately $3.00 per share.

Assuming Bitcoin holds near its current price and factoring in modestly declining revenues from the core healthcare business, I estimate Semler’s fair value to be closer to $36 per share, a slight discount to its current trading value.

I’ll note that this valuation also excludes the value of long-term investments and long-term notes receivable which adds approximately $2 million more in assets.

Ok, so with the basic thesis out of the way, let’s dive a little deeper into Semler Scientific including its operations, risks, recent events, and its outlook both from an operational standpoint and in light of its newly adopted treasury strategy.

Operations

Semler Scientific generates the majority of its revenue through the licensing of its QuantaFlo vascular testing product, which is primarily used by healthcare insurers, physician groups, and risk assessment providers. The company employs a subscription-based SaaS model, offering QuantaFlo under fixed monthly fees or per-test pricing structures. This recurring revenue approach reduces the upfront capital investment for customers and promotes steady, predictable cash flow for Semler. The system is typically deployed in primary care and in-home settings, where ease of use and portability are critical. Key drivers of revenue include the number of tests performed by healthcare providers and the broader adoption of vascular screening within preventive health programs, especially those targeting Medicare Advantage populations. Insurance coverage, particularly within Medicare Advantage, indirectly influences demand for QuantaFlo, as the test aids in risk adjustment coding and supports preventive care efforts that align with reimbursement incentives for providers and insurers.

Semler reported $56.3 million in revenue for 2024, down from $68.2 million in 2023. This decline was primarily driven by significant headwinds in its core diagnostic business, including adverse reimbursement changes and shifting payer policies. Notably, the Centers for Medicare & Medicaid Services (CMS) removed the risk adjustment benefit for peripheral arterial disease (PAD) diagnoses without complications, reducing the financial incentive for Medicare Advantage plans to conduct routine screenings using Semler’s QuantaFlo device. In addition, private insurer Aetna reclassified digital (ABI) tools like QuantaFlo as experimental, rendering them non-reimbursable and further dampening provider adoption. The company’s heavy reliance on a small number of customers, two of which accounted for over 70% of revenue in 2024, also underscores its revenue concentration risk. The situation deteriorated further in the first quarter of 2025, with revenue declining 44.4% year-over-year and operating margin falling to -15.3%. This was driven by reduced product utilization, a $29.75 million one-time legal settlement tied to a Department of Justice investigation, higher ongoing legal expenses, and increased investments in engineering and product development as the company attempts to pivot its platform and stabilize future revenue streams

Strategy: Semler’s operational strategy is focused on expanding their customer base by adding new medical clinics, growing among value-based care providers, and targeting new markets that would benefit from testing. The company is seeking additional FDA 510(k) clearance to broaden QuantaFlo’s reach beyond peripheral arterial disease to other cardiovascular conditions.

Sales and Marketing: Sales and marketing efforts are directed toward healthcare systems and payors, with an emphasis on demonstrating the value of early disease detection. They aim to target customers with patients at risk of developing PAD and other cardiovascular diseases. According to the company 10K this includes people over the age of 50, African Americans, smokers, and populations with diabetes, high blood pressure, high cholesterol, and history of heart attack or stroke.

QuantaFlo is sold through a direct sales force, and customers receive brief online or in-person training upon installation. The company offers both fixed-fee and usage-based licensing models, with flexible billing options. Technical support is available daily, and software updates are delivered electronically as needed.

Manufacturing: Manufacturing is outsourced to U.S. based third-party contractors responsible for component assembly, quality control, and distribution, allowing the company to remain asset-light and scalable. Some vendor components are sourced from China, and related costs may be affected by tariffs. However, Semler has indicated that alternative suppliers are available to mitigate potential supply chain disruptions.

Other Products, Services, & Investments: In addition to QuantaFlo, Semler has made several minority investments in healthcare technology companies. These include SYNAPS Dx, the developer of Discern, a test designed to assist in the diagnosis of Alzheimer’s disease, and Monarch Medical Technologies, which offers EndoTool, a clinical decision support software for inpatient insulin dosing. Semler previously held a distribution agreement for Insulin Insights, a diabetes management software developed by Mellitus Health, but the product was discontinued due to limited market adoption. These investments currently do not contribute materially to the company’s revenue but reflect Semler’s interest in adjacent areas of chronic disease management.

QuantaFlo: QuantaFlo is Semler’s flagship product. The device uses a sensor clamp placed on a patient’s fingers and toes to emit infrared light, which reflects off red blood cells to generate a real-time waveform analyzed by proprietary software. The entire test takes about five minutes, with each limb assessed in roughly 30 seconds. Unlike traditional ankle-brachial index (ABI) tests that require trained vascular technicians and blood pressure cuffs, QuantaFlo can be operated by general clinical staff without specialized training. It is portable, compatible with common operating systems like Windows, iOS, and Android, making it easy to use in both clinical and home settings. Its ease of use, speed, and ability to detect PAD even in asymptomatic patients make it an efficient and accessible diagnostic tool. As stated in the introduction, Semler licenses QuantaFlo on a subscription or per-test basis, lowering upfront costs for healthcare providers and promoting broader adoption. The fee-for-service structure can also incentivize physicians to provide more treatments on the basis that they are paid more on quantity of care, rather than quality of care.

Operational Outlook

The core business operations of Semler Scientific have faced significant headwinds in the past year. Outlook remains mixed and overall uncertain. The following are factors that I expect will impact the company over the next few years.

Patent Expiration: QuantaFlo is protected by U.S. Patent No. 7,628,760, which covers its core diagnostic technology and expires on December 11, 2027. The patent’s expiration may allow competitors to develop similar products. Semler has noted that its market position, proprietary software, and potential additional patents may help mitigate competitive risk. I expect and have modeled for a continued decline in revenues.

Reduced Screening Incentives: A recent policy change by the Centers for Medicare & Medicaid Services (CMS) eliminated risk adjustment benefits for peripheral arterial disease (PAD) diagnoses without complications, reducing the financial incentive for Medicare Advantage plans to conduct routine PAD screenings using QuantaFlo. Compounding this, private insurer Aetna reclassified digital ABI tools like QuantaFlo as experimental and non-reimbursable, significantly curtailing provider adoption due to lack of coverage. These developments have materially impacted demand for Semler’s core product, driving a decline in revenue since 2023, a trend expected to persist through 2025, placing continued pressure on the company’s traditional operations.

DOJ Suit: Semler Scientific is currently involved in a Department of Justice investigation related to the marketing and use of its QuantaFlo device in Medicare Advantage populations. The DOJ alleges that QuantaFlo contributed to inflated diagnoses of peripheral artery disease, leading to higher patient risk scores and increased federal reimbursements to insurers. In April 2025, Semler agreed in principle to a $29.75 million settlement, though the agreement is not yet finalized and further legal action remains possible. The investigation has raised concerns about industry practices and has negatively impacted the company’s stock price and outlook. If the settlement is not finalized, the company could face additional reputational harm and may be exposed to further legal and regulatory risks, including potential suspension from government healthcare programs. This could also undermine investor and customer confidence.

New 510K Clearance: The company is pursuing 510(k) clearance to expand QuantaFlo’s approved use to include the diagnosis of additional cardiovascular conditions. While Semler anticipates a decision in the first half of 2025, no clearance has been received to date. In the interim, the company is test marketing other FDA-cleared cardiovascular products that may align with customer needs and currently has three additional U.S. patent applications under review.

Competition: QuantaFlo’s main competition is the standard blood pressure cuff ABI device. While ABI remains the preferred option for confirmatory diagnostics in clinical vascular settings, QuantaFlo holds advantages in ease of use, portability, shorter testing time, reduced subjectivity, and less reliance on trained technicians. Competing digital devices are beginning to enter the market with the goal of providing faster and more objective results. It is currently uncertain how QuantaFlo will compete with these emerging alternatives.

Customer Outlook: The growing emphasis on preventive care and early disease detection aligns well with QuantaFlo’s clinical use case. As healthcare systems increasingly prioritize early intervention to “improve outcomes and reduce long-term costs,” tools like QuantaFlo are positioned to benefit from broader adoption. The rising prevalence of chronic conditions such as diabetes and cardiovascular disease, both major risk factors for peripheral arterial disease, further underscores the need for accessible vascular screening solutions. This of course assumes that QuantaFlo remains a viable and reliable option.

Convertible Bond Offering: In January 2025, Semler Scientific completed a $100 million convertible bond offering, issuing 4.25% senior notes due in 2030. The company received approximately $91 million in net proceeds, which it plans to use for general corporate purposes, including continued investment in Bitcoin. While the offering strengthens Semler’s liquidity and provides financial flexibility, it introduces long-term risks. If the company’s share price exceeds the conversion price of $76.44, bondholders may convert their notes into equity, potentially diluting existing shareholders. To mitigate this, Semler entered into capped call transactions to mitigate dilution up to a share price of $107.01, dilution beyond that level remains a possibility. Additionally, the company now faces a recurring interest obligation, representing a shift from its previously debt-free capital structure.

Bitcoin Strategy and Outlook

If you have read this far then I don’t expect I have to sell you on Bitcoin. My goal here is simply to lay out some of the recent trends in Bitcoin that are likely to result in an increased USD value and increased valuation for Semler over the next six months to a year.

As illustrated above, the company’s stock price currently trades near the NAV of Semler’s treasury assets including Bitcoin, cash and cash equivalents and short-term notes. Providing investors with a highly cash generative operating business at a slight discount. Over the past 5 years, the CAGR of Bitcoin was 65%. Although I anticipate further volatility in the asset, there are several reasons I expect it will be higher six months to a year from now.

Increased Institutional Adoption: Governments are increasingly exploring the idea of establishing strategic Bitcoin reserves, while companies are showing growing interest in holding Bitcoin as a treasury reserve asset. This trend toward broader institutional adoption is expected to drive additional demand for Bitcoin, contributing to upward pressure on its price. As of early June, The White House has hinted towards the purchase of Bitcoin in interest of building up the U.S.’s strateguc reserve.

Decreasing Supply of Bitcoin Across Exchanges: I am sure we have all seen this chart at some point showing that the supply of Bitcoin held on exchanges is dwindling. This is likely an indication that people and institutions are moving their Bitcoin off of exchanges and into cold wallets suggesting bullish sentiment. At some point this is likely to result in a supply shock increasing volatility and sending the price higher. The chart below is from Cryptoquant.com dated June 8th. Note that the data for supply lags price data by a month.

Increased Mainstream Acceptance and Education: Pretty self-explanatory. Countries such as Russia and China are accepting they cannot suppress Bitcoin adoption. More investment firms and their customers are showing an interest in it. And there is more education available for people.

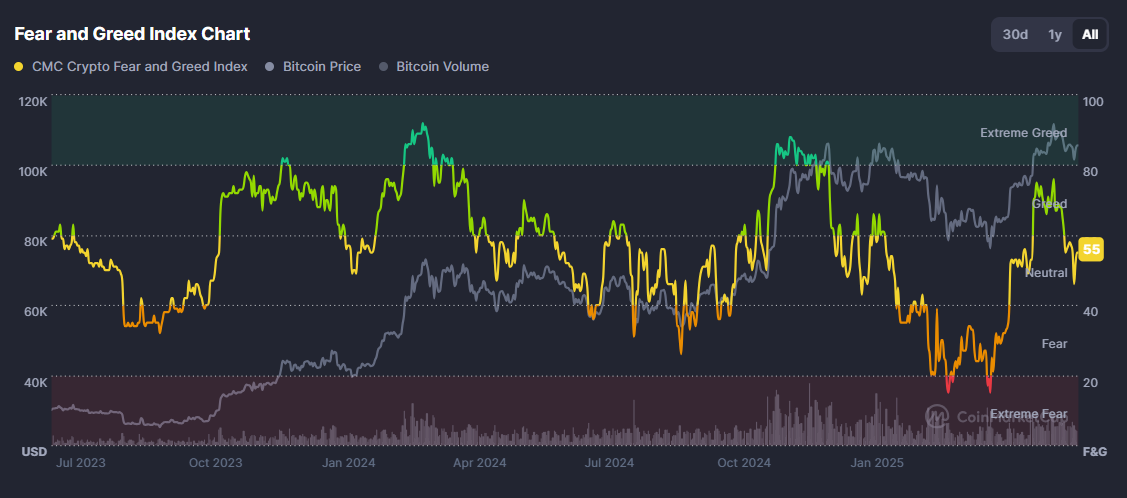

Market Sentiment on the Fear/Greed Index: When I originally wrote this, Bitcoin sentiment was in the extreme fear zone. As of today, it has moved into more neutral territory, but I’m including the chart and link in case similar conditions return. I regularly use the Fear & Greed Index for equities, where it’s been a useful tool for gauging sentiment and identifying potential entry points. While crypto-focused versions of this index don’t yet have the same track record, the concept still applies. Periods of fear often coincide with lower prices and potential undervaluation. The chart below, from CoinMarketCap.com as of June 8th, reflects the current state of sentiment in the Bitcoin market.

Strategy and Treatment

Semler has proclaimed itself a Bitcoin first company and plans to continue accumulating Bitcoin using cash generated from operations and proceeds from future at-the-market (ATM) equity offerings, with additional convertible debt offerings also under consideration. The company has elected to early adopt ASU 2023-08, a new FASB accounting standard requiring Bitcoin and similar crypto assets to be measured at fair value at the end of each reporting period. As a result, Semler’s reported net income and EPS may experience significant volatility due to fluctuations in Bitcoin’s market price, although this will not affect cash flow from operations.

When I first wrote this in early April, market sentiment was deeply negative, and Semler’s Bitcoin holdings were trading at an unrealized loss. According to its latest 8-K, the company now holds 4,449 Bitcoin at an average cost basis of $92,158 per BTC, resulting in a substantial unrealized gain at current prices. While no tax liability is incurred unless the Bitcoin is sold or otherwise disposed of, investors may apply a discount to Semler’s stock relative to the net asset value of its Bitcoin treasury to account for potential future taxes or liquidity risks. Semler holds its Bitcoin through custodial arrangements with Coinbase and NYDIG, and recently entered into a Master Loan Agreement with Coinbase, enabling it to borrow cash or digital assets using its Bitcoin as collateral.

Expectations and Risks:

While Semler has adopted a Bitcoin-first strategy similar to MicroStrategy, it is unlikely to trade at the same premium any time soon. MicroStrategy benefits from greater scale, broader brand recognition, deeper trading liquidity, and a more established financing strategy. In contrast, Semler faces a different set of risks; most notably the potential for additional legal liabilities and continued disruption to its core operations. These challenges could limit its ability to generate sufficient free cash flow to acquire additional Bitcoin or meet future debt obligations.

As of this writing on the eve of June 9th, the slight discount between the current price of Semler’s common stock and my valuation is small. Depending on one’s strategy it may arguably be more worthwhile to just buy Bitcoin itself. One just has to take into account fees and their long-term goals. The main reason I am writing this up is in the event the valuation gap increases and provides an opportunity for loose cash with a slightly higher upside when valuation normalizes.

That said, there may be opportunities for the stock to trade at a premium, particularly in the event of a short squeeze. The latest short-term interest data estimates that approximately 1.8 million shares are sold short representing about 13.5% of shares outstanding and roughly 16% of the estimated float. With an average daily trading volume of around 663,000 shares, the estimated days to cover stands at just over three days, a modest figure, but one that’s still meaningful in the context of a tightly held float. Again, it’s something to take note of.

Conclusion:

This is a fast-moving idea that requires patience and above-average vigilance to capitalize on effectively. For investors who believe in the long-term value of Bitcoin, Semler offers a unique way to gain exposure through an equity structure, with limited downside beyond the inherent volatility of Bitcoin itself. At the same time, it presents the potential for opportunistic exits at a premium, particularly in the event of favorable sentiment shifts or a Bitcoin run.

Thanks for reading.

Interesting to see the Bitcoin reserve. Quite a large stack!