Array Technologies Inc. Deep Dive and Valuation ($ARRY)

Array Technologies is the number two global leader in the manufacturing and supply of solar trackers used in utility and distributed generation solar energy projects.

Array Technologies Inc. specializes in the manufacturing and supply of ground-mounted solar tracking systems used in utility and distributed generation solar energy projects. Solar tracking systems are mounting devices that automatically move solar panels throughout the day, so they continuously face the sun, optimizing their exposure to sunlight and thereby increasing efficiency and energy production. Solar energy projects using trackers typically generate 10% to 25% more energy and deliver around 5% lower Levelized Cost of Energy (LCOE) than projects that use “fixed tilt” mounting systems, which are stationary mounting systems. Array Technologies has a global presence, and ranks as the second largest solar tracking company in the world behind NexTracker Inc. They predominantly cater to utility-scale solar project developers, independent power producers, and directly with utility companies themselves.

Array Technologies Inc. was founded in 1989 in Albuquerque New Mexico, by Ron Corio, a pioneer in solar engineering and mechanical design. Since the beginning, the company has focused on manufacturing ground-mounting tracking systems used in large-scale solar energy projects. In October of 2020, Array IPO’d on the NASDAQ under the ticker symbol ARRY. Funds from the IPO were used to pay down an existing credit facility and growth. As of September 2024, Array employed 961 full time employees across The United States, Europe, Latin America, Africa, Australia, and Asia. The company appears to be well-positioned to benefit from continued growth in solar adoption and its ability to provide value enhancing-solar tracking solutions to large-scale solar projects globally.

Operations

Revenues

Array Technologies derives revenues from the sale of its tracker systems and associated services. Before we dive into their different tracker system offerings let’s establish how their systems work and some of the definitions. Array Technologies primarily caters to large-scale solar projects, often referred to as solar farms. A solar array, which is a collection of multiple solar panels or modules linked together, generates electricity by harnessing sunlight. Essentially, a solar farm comprises several of these solar arrays. Typically, solar arrays are constructed in rows oriented in a north-south direction, enabling single-axis tracking systems to pivot east-west, efficiently following the sun’s daily path across the sky. An array can have dozens of rows with more than 100 panels in each row. Refer to the linked YouTube video for a quick overview of solar farm construction. When developing solar farms, it is crucial to evaluate factors such as terrain, seasonal weather patterns, sunlight exposure, soil stability, and grid integration in deciding what tracking system is appropriate for a project. Array Technologies only specializes in single-axis tracking systems as opposed to dual-axis systems, which adjusts solar panels both vertically and horizontally to follow the sun’s path across the sky. Due to their higher construction and maintenance costs, mechanical complexity, shorter life spans, and challenges in adapting to uneven terrains, dual-axis trackers are often not considered ideal for large-scale solar projects. Single-axis systems are simple, scalable, more cost effective, can be more easily adapted to changes in terrain, and have longer lifespans, which is about 30 years for Array’s product lines. It is estimated that over 70% of new utility-scale solar farm projects are using trackers.

Array Technologies offers three different tracking systems, each designed to be optimally suited to the specific needs and conditions of diverse solar projects.

1. Dura Track HZ v3: The Dura Track HZ v3 is Array’s flagship product known for its exceptional reliability, simplicity, and low maintenance needs. Dura Track is on its third generation and includes patented features such as a single-bolt per module mounting system that reduces installation time and increases reliability with fewer moving parts. The Dura Track utilizes a centralized architecture that can operate up to 32 linked rows on a single motor compared to the decentralized architecture of most competitors who use a motor for each row which is more costly. This gives Array a competitive advantage in terms of cost and results in lower maintenance costs over the life of the project. Dura Track also has a built in wind-mitigation system to protect from adverse weather conditions.

2. Array STI H250: The Array STI H250 is Array’s dual-row tracker acquired through their 2022 acquisition of STI Norland, a European manufacturer of solar trackers. It is Array’s lowest cost option, meant to appeal to cap-ex sensitive customers with quick and seamless installation. The Array STI H250 is designed with one motor capable of moving up to 120 modules and is well suited for sloped grounds, field obstructions, and fragmented or irregular boundaries.

3. Array OmniTrack: The Array OmniTrack is essentially an upgraded version of the DuraTrack, constructed with more robust materials and designed for deployment on uneven terrains with steeper slopes. OmniTrack allows for up to 1% north-south slope change in torque tubes which is the best in the industry. Its flexible architecture minimizes ground disturbance, helping to navigate environmental regulations more effectively, reduce grading and material costs, and maximize site usage and production efficiency. Terrain previously deemed unsuitable for solar projects, or that would have incurred substantial grading expenses, can now be viably utilized.

Array’s tracking systems are designed to be versatile and adaptable, capable of supporting various types and sizes of photovoltaic modules. This adaptability is crucial for utility-scale solar installations, which may use different panel technologies depending on the project's specific requirements, geographic location, and cost considerations. For more information on Array’s Tracker systems and their benefits, check out the 2023 Investors Day Presentation.

In addition to its tracking systems, Array Technologies offers an advanced tracker module called Skylink, which integrates seamlessly with both the DuraTrack and OmniTrack systems. Skylink enhances performance by utilizing wireless communication technology to reduce costs, ensures robust responses to extreme weather conditions, and employs backtracking to minimize shading effects. Array Technologies also provides a suite of software and control-based products known as SmarTrack, specifically designed for utility-scale solar sites. This software leverages both historical and real-time data, site-specific weather and energy production data, along with machine learning algorithms, to optimize the positioning of solar arrays for maximum energy production. Additionally, SmarTrack includes advanced features such as hail alert responses, snow management, backtracking capabilities, and strategies for optimizing output during overcast conditions.

The last notable source of revenue for Array is services. Array offers field services and training programs to help meet the needs of engineering, procurement and construction firms (EPCs), utility-scale solar, operation and maintenance partners, and solar site developers. Providing these services has enabled Array to reduce operational downtimes and increase levels of productivity and work quality in the field.

Manufacturing and Supply Chain

Array Technologies operates a 58,000 square foot facility in Albuquerque, New Mexico, and is currently constructing a second facility in the state, partially funded by the Inflation Reduction Act and the Local Economic Development Act. Following their STI acquisition, Array also manages manufacturing and warehouse facilities spanning 54,000 square feet and 632,000 square feet in Spain and Brazil.

Array's operational strategy across these facilities is designed to achieve several key objectives. They aim to limit capital-intensive and low value-added activities by outsourcing them, minimize labor content wherever feasible, reduce the assembly requirements for customers at project sites, and decrease material handling both from vendors to the facilities and within the facilities themselves. At their Albuquerque facility, Array produces and/or assembles module clamps, center structures, and motor controller assemblies, while outsourcing components like steel tubing, steel supports, drivelines, bearing assemblies, gearboxes, electric motors, and electronic controllers. These components are directly shipped to warehouses or customer job sites. Despite relying on a small group of vendors for certain parts, which introduces a risk, Array has identified alternative vendors to ensure continuity and is capable of internally producing some of these components if necessary. In a supply disruption situation, it is likely the company would take a margin hit. This operational strategy enables Array to maintain a relatively asset-light business model, minimizing certain fixed costs. It supports effective scalability and enhances cyclical resilience during market downturns. However, this approach requires the company to sustain a robust logistics and supply chain system to meet customer demands, along with reliable access to a diverse range of vendors. It can also give them less control over costs.

The majority of Array Technologies' products are manufactured using hot rolled coil steel (HRC steel) and aluminum, making the business significantly vulnerable to fluctuations in commodity prices. While some of these costs can be passed on to customers, it operates in a price-sensitive market where higher capital costs, such as those for steel, can diminish project returns or reduce overall demand. The ability of Array to balance its profitability against periods of rising costs is crucial to its success. Historically, the company has shown a willingness to yield market share to competitors during volatile periods when it was not confident in maintaining certain levels of profit margin.

Customers and Sales

Array’s customers consist of developers, independent power producers, EPCs, utilities, independent engineering firms, insurers and mechanical subcontractors. In 2023, EPCs represented 69% of revenues in line with historical averages. It is not uncommon for over 10% of sales to go to a single customer, however it is worth noting that this number is representative of multiple different end projects with different end customers and separate financing. Array’s sales and marketing strategy combines direct sales initiatives with independent third-party studies, and active engagement through training seminars and sponsorship of key industry conferences and events. Their goal is to educate all critical influencers and stakeholders involved in the construction, ownership, and maintenance of solar projects, emphasizing the superior benefits and the low lifetime ownership costs of their products.

Array Technologies collaborates with leading EPC contractors such as RP Construction Services, Swinerton Renewable Energy, and Blatter Energy for the design, procurement, and construction of solar projects. Essentially, Array enters into supply agreements with these firms, providing them with the necessary technology and products. The EPC contractors then integrate these components into their solar installations. These partnerships are vital for Array, as they serve as direct sales channels for their products, ensuring a steady demand and broader deployment of their solar tracking systems.

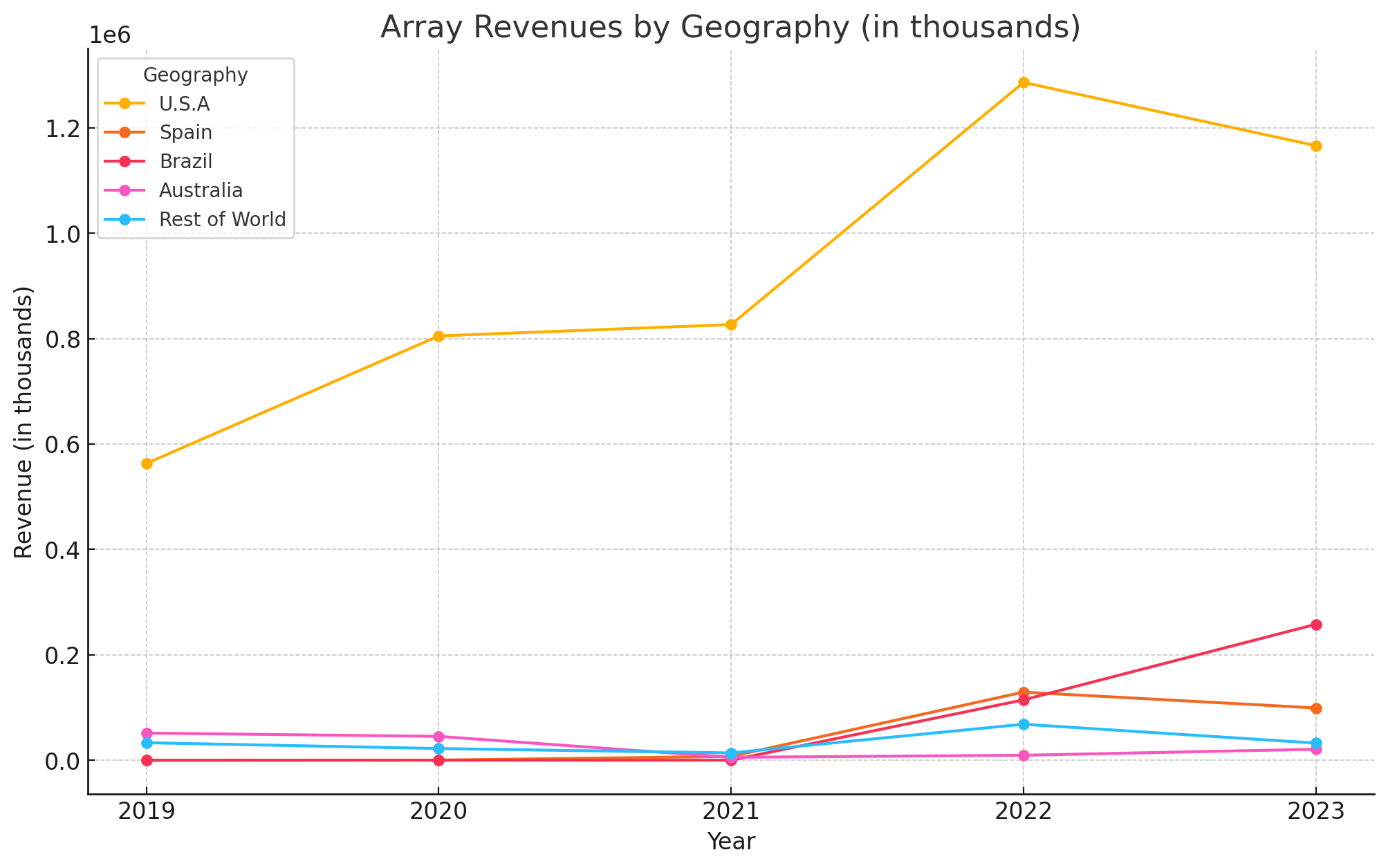

Array provides revenue data for four major customer markets including the United States, Spain, Brazil, and Australia. In the latest 10Q filing the company states they have and active sales presence in the U.S., Spain, Brazil, South Africa, Australia, and the U.K. In fiscal 2023, revenues in the United States were $1.166 billion (74% of total), followed by Brazil at $257.8 million (16.4%), and Spain at $99.2 million (6.2%). During the fiscal year, Array shipped more than 73 gigawatts of trackers to customer worldwide, up from 58 gigawatts in 2022.

Acquisition of STI Norland and Other Investments

In 2022, Array Technologies acquired STI Norland, a European manufacturer of solar trackers that, at the time, held the number one market share in Brazil. This acquisition expanded Array’s product portfolio to include a dual-row tracker system designed for irregular terrain and regions with low wind or snow load requirements. Leveraging STI Norland's established presence in Spain and Brazil, Array aimed to enhance its legacy offerings and bolster its global footprint. However, the acquisition has not been without challenges. In Q3 2024, Array recorded a $162 million goodwill impairment related to the STI acquisition, primarily due to underperformance in key markets, most notably Brazil. Factors contributing to this underperformance included challenges in integrating STI Norland's operations, lower-than-anticipated revenue growth, and evolving market conditions that affected the profitability of the combined entity. In Brazil, Array has since lost market share to their largest competitor Nextracker and others. One thing to note with market share in this industry is that it is a large project business, where a few projects can have an outsized impact on shorter term views of share. Looking at market share over a longer time frame such as a few years provides a more informed picture.

In November 2024, Array announced its participation in a pre-Series A funding round for Swap Robotics, contributing $3 million initially, with an additional $2 million to be invested upon the achievement of specific milestones. Swap Robotics specializes in developing and manufacturing electric robots designed for cutting vegetation. Effective vegetation management is crucial for maintaining operational efficiency, safety, and longevity of solar farms, as well as maximizing sunlight exposure. This becomes even more essential with the increased adoption of bifacial panels, where vegetation control is critical to optimizing panel efficiency. Swap Robotics, claims that their offerings reduce operational costs by 10% - 20%. I expect their use is limited to installations with relatively level terrain. I found the initial press release somewhat misleading, as it seemed to suggest that the investment was related to the actual installation of panels. While I see potential for Array to expand its horizontal offerings with Swap Robotics, I remain skeptical about the benefits of this investment. On the day the announcement was made, Array's stock fell by over 7%.

The Solar Tracker Industry

The solar tracker industry is notably complex, with projected growth rates varying widely—from mid-single digits to mid-twenties—over the next decade. Personally, I do not feel it is appropriate to make projections off speculative research reports. As I develop my valuation for Array, I find it is one of those companies where we are best off reverse engineering for our desired outcome and understanding what growth rates and industry factors must play out to achieve this outcome. As a result, my analysis in this section will focus on identifying the key drivers of demand for solar projects, exploring macro trends that are likely to propel growth, and competition.

Factors that Influence the Industry

One of the challenges in projecting growth in the solar tracker industry is accurately forecasting the costs of essential commodities like steel and aluminum, which are crucial for manufacturing solar trackers. Additionally, factors such as fuel costs for shipping, the price of solar panels, and electricity rates also need to be considered. The demand for large-scale solar projects, which typically utilize solar trackers, is highly sensitive to these costs. For instance, if steel prices increase, the cost of producing solar trackers rises, potentially leading to a decrease in demand. Conversely, when electricity costs are high, solar projects become more economically viable, presenting a more attractive and often more predictable alternative to traditional power sources. Solar projects involve significant initial capital expenditure, and their feasibility hinges on achieving an attractive Levelized Cost of Energy (LCOE) and a favorable return on investment. This complexity makes projecting growth figures difficult unless costs can be reliably predicted.

Other factors that drive demand in the industry include government incentives, demand for electricity, environmental concerns, and green energy targets. There are several federal, state, local and foreign government bodies that provide incentives to owners, end users, distributors and manufacturers of solar energy systems. These incentives typically come in the form of rebates, tax credits and other financial incentives such as system performance payments. One of the most notable incentives impacting solar tracking companies is the 45X Credit included in the Inflation Reduction Act (IRA) which aims to incentivize domestic manufacturing. “The 45X Credit is a per-unit tax credit that is earned over time for each clean energy component domestically produced and sold by a manufacturer.” Array is expected to recognize over $40 million in reduced costs as part of this credit program through 2024. The 45X Credit is expected to phase down in 2030 and completely out in 2032. Other incentives are available on state and local levels as well as those in foreign markets. These incentives are expected to increase the viability of solar projects and increase their demand. In the United States there are concerns that the Trump administration policies will hurt the renewable energy industry or claw back some of the government incentives. I personally do not believe this is a huge concern. Solar companies and solar component companies performed well under the previous Trump administration and his policies generally promote energy independence for the United States. If solar can maintain itself as a viable, cost-effective option I anticipate demand will continue to grow. Additionally, there remains bipartisan support in congress to support the protection of energy tax credits portion of the IRA.

Many of these incentive programs are being driven by environmental concerns and green energy targets set by various global entities. I could sit here and name off various environmental acts, pledges and ambitious targets, but at the end of the day its mostly bureaucratic virtue signaling. Nonetheless, it is a force driving demand in the industry. Should there be a reduction in government incentives, it is likely that demand in the industry would also decline.

Industry Trends

In the above section we discussed some of the factors that have an overall influence on the industry. Now I will focus on some of the overall industry trends and how these are likely to spur further growth. From 2018 to 2022 the U.S. solar tracker industry grew at a CAGR of 8.8%. Over the past decade, the cost of solar panel modules has decreased approximately 70% to 80%, primarily as a result of improved photovoltaic technology (PV) and manufacturing scale. This decline in costs has substantially increased the viability of projects, making them a more appealing alternative, a trend that will likely continue.

The solar industry is poised to benefit significantly from the rising demand for electricity over the next decade. In Q3 of 2024, solar power accounted for 64% of all new electricity-generating capacity added to the U.S. grid, surpassing any other source. Factors contributing to this growing demand for electricity include the increased adoption of electric vehicles (EVs), technological advancements in data centers and manufacturing, population growth, and broader economic expansion. To support the expanding electrical grid capacity, large solar projects, many equipped with tracking systems, will be essential. Demand for utility scale solar projects is expected to continue moving forward.

Improved technology in areas of energy storage is also a notable trend. Improved energy storage technology is set to enhance utility-scale solar projects by enabling more consistent and reliable electricity supply, regardless of solar variability. By storing excess energy produced during peak sunlight hours and releasing it as needed, storage technologies help stabilize the grid and extend the usability of solar power into nighttime or cloudy periods. This capability not only increases the economic value of solar projects by allowing them to sell power at optimal times but also bolsters grid integration, making solar a more competitive and reliable energy source. As a result, improved energy storage is likely to increase solar adoption and demand so the necessary components.

Technological advances such as bifacial panels are also making solar projects more viable. Bifacial panels are PV panels that can capture sunlight on both their front and rear sides. Unlike traditional monofacial modules that only absorb sunlight on one side, bifacial modules take advantage of reflected light from the ground and other surfaces, thereby increasing their energy output. According to data collected by the International Energy Agency (IEA), bifacial tracking systems that utilize single access trackers increase energy output by between 20% and 35% on average compared to conventional systems. Projects that utilize bifacial panels come with additional considerations. The efficiency of bifacial panels partly relies on their ability to capture reflected light from the ground. Consequently, features like backtracking capabilities in solar tracking systems become crucial. Moreover, bifacial panels typically require greater spacing between rows, requiring greater land use, and are often positioned higher off the ground compared to conventional systems, necessitating more materials which increases cost. All in all, bifacial panels are a notable advancement in solar technology. The IEA forecasts that by 2033, bifacial modules will account for more than 70% of the market.

For more information on recent trends check out The Solar Energy Industries Association who puts out a quarterly report offering insights into market trends.

Competition

The solar tracker industry is dominated by a limited number of companies, largely because trackers are highly specialized products that require unique expertise to design. Additionally, reputation plays a crucial role in this industry, where customers often hesitate to adopt unproven products and prefer to rely on companies with decades of proven experience. This dynamic creates barriers to entry, making it challenging for newer firms to compete and scale effectively.

Solar tracker companies typically compete based on several key factors: established track records of product performance, system energy yield, software capabilities, product features, total cost of ownership and return on investment, reliability, customer support, product warranty terms, and services. Despite the presence of only a few firms, the solar tracker industry remains quite fragmented, often leading to significant price competition among competitors.

Array Technologies is the number two player in the solar tracker space. Their direct competition includes Nextracker Inc., GameChange Solar, PV Hardware, FTC Solar, Arctech Solar and Soltec. Array also competes indirectly with manufacturers of fixed mount systems such as UNIRAC Inc. and RBI Solar Inc. In the grand scheme of things, all of these companies are competing with providers of conventional and renewable energy alternatives such as coal, geothermal, nuclear, natural gas and wind.

Nextracker is by far Array’s largest competitor. Nextracker has a much broader international presence compared to Array with significant market share in Latin America, Australia, the Middle East, and Asia in addition to North America. Both companies specialize in highly reputable single-axis trackers but differ in their approach; Array Technologies focuses on mechanical simplicity and durability, while Nextracker emphasizes technological integration and smart functionality. In recent years, Nextracker has experienced a fairly consistent growth in revenues, in contrast to Array Technologies, whose revenues have declined from their peak in 2022.

Competitive Advantages

Array Technologies benefits from a handful of competitive advantages. I would not consider some of these to Buffett level – durable competitive advantages but they have earned Array a number two spot for solar tracking companies in the world. The following competitive advantages I have identified.

Brand Strength: Array Technologies has been developing and manufacturing solar trackers for 35 years, establishing a strong reputation for efficient and reliable solutions. Customers prioritize reputable companies with proven products over those offering untested alternatives when designing and constructing solar projects. Array's brand strength, combined with its position as a major player benefiting from economies of scale, creates significant barriers to entry, discouraging new competitors from entering the market.

Economies of Scale: As a number two player in the industry, Array benefits from a degree of economies of scale in which it can manufacture and or secure better pricing for components due to their higher volume of production.

Product Differentiation: Ultimately, customers select products based on their specific needs. However, companies can differentiate themselves through the unique value of their offerings. Array has set itself apart by delivering simplified, reliable, and low-maintenance solar tracker solutions. As mentioned prior, Array utilizes a centralized architecture design in which several rows are controlled by a single motor compared to the decentralized architecture of most competitors who use a motor for each row. This design reduces the number of components, minimizing points of failure, reduces maintenance costs, lowers capital costs for projects, and is more scalable. Historically, these solutions have provided a highly competitive Levelized Cost of Energy (LCOE) and lower fixed operation and maintenance costs compared to competitors. (I will note that a decentralized design such as Nextracker’s, can be beneficial for installations on uneven land or in large fields where shading and terrain can vary significantly across the site, but it is more costly due to the use of more components and necessary maintenance.) Array’s holds a patent on their linked-row, rotating gear drive system through 2030, and believes this is competitive advantage to them. In addition, Array's products are solar panel agnostic, making them compatible with most solar panel brands across the industry. They also enhance efficiency by offering competitive data and software solutions integrated with their trackers.

Operations: Array operates assets-light business model where the majority of the manufacturing is handled by third party vendors. This model allows Array to remain flexible, reduce fixed costs, and scale operations more effectively. By avoiding the heavy capital investments associated with owning and operating large manufacturing facilities, the company can allocate resources to innovation, customer service, and maintaining a strong supply chain. It also gives Array cyclical resiliency in the event of market downturns. The downside of this operating style is that is requires a robust logistics system and reliable access to a diverse network of vendors to ensure consistent product quality and timely delivery. Many of Array’s competitors operate on a similar model. Array has historically maintained a strong U.S. based supply chain which boasts well for them in areas of tariffs. Array has historically maintained a U.S.-based supply chain, which positions the company favorably in managing tariff-related challenges.

Risks

Array’s business model is exposed to a range of risks. Below, I’ve outlined what I believe are some of the most significant to our investment thesis:

The viability and demand for solar projects are highly price-sensitive. Rising costs in steel, aluminum, fuel, and logistics could negatively impact revenue by reducing demand for solar installations. Furthermore, challenges in sourcing critical components for tracker construction could lead to project delays or budget overruns, ultimately harming margins and damaging the company’s reputation. Array experienced several customer pushouts during 2023 and early 2024 due to pricing concerns.

A decline in the retail cost of electricity or reduced costs associated with alternative energy sources, such as coal, natural gas, wind, hydro, geothermal, or nuclear power, could make solar projects less economically viable, leading to decreased demand. I do not believe nuclear energy poses a significant competitive threat at this time, except in regions where it is already well-established. The construction and integration of nuclear facilities into the grid typically take many years, limiting its immediate impact on the market.

A reduction, elimination, expiration, or delay in government incentives for solar energy projects could lead to decreased demand or even project cancellations. I do not believe this will be an issue and take a contrarian stance that the Trump administration and its energy independence aimed policies will be beneficial to the overall industry allowing for continued growth of solar.

Currency fluctuation may negatively impact Array’s results. Although the majority of their revenues are within the United States, the company is expanding into other markets and fluctuations in currency may have a greater impact on the company moving forward.

Tariffs and escalating global tensions could increase costs or complicate the procurement of key components for solar trackers. Array is dependent on a number of outside vendors. Although many of these vendors are located within the United States, failure of these vendors to deliver would have an adverse impact on Array’s results.

Underperformance of acquisitions and other investments. As mentioned earlier, Array took a $162 million goodwill write off related to their STI acquisition. I anticipate this will be a one-time payment, but it has weakened my confidence in management. Although it is small, I remain skeptical of the investment in Swap Robotic and how that may benefit shareholders. Array is currently taking actions to address material weaknesses in their internal controls.

Shareholders of Array face a risk of their own. Array has $425 in convertible senior notes due 2028. These notes are convertible into common shares at a rate of approximately 41.9054 shares per $1,000 principal amount, equating to around 10.1 million shares if fully converted. The exercise price for these convertible notes is $23.86 per share, about 4x the current value of the stock and quite a bit higher than my fair value estimate as you’ll see. Nonetheless, shareholders do face a degree of dilution in the event these notes are exercised. Array is utilizing capped calls to offset some of this dilution risk.

Other risks that Array may face in the course of business include cyber-attacks, manufacturing disruptions, the ability to protect intellectual property, failure to maintain relationships with key vendors, and damage to reputation resulting from operational issues or product failures. The company carries long-term debt totaling $648.3 million. Of this, $235 million is under a secured credit facility, while $425 million consists of convertible notes. Additionally, Array holds $33 million in other debt obligations acquired through the STI acquisition. This portion of the debt is denominated in euros, with annual interest rates ranging from 3.63% to 4.53%. As of their Q3 2024 10-Q filing, Array reported $332.3 million in cash on its balance sheet. Given this cash position and the company’s cash flow levels, I do not anticipate any issues in meeting its debt obligations.

Management

Executive Management

Array has undergone several changes in Executive Management in recent years, reflecting a period of transition for the company. Kevin Hostetler, the current CEO, succeeded Jim Fusaro following his retirement in April 2022. Hostetler brings over 18 years of leadership experience across engineered product and service companies, including FDH Infrastructure and IDEX Corporation. Neil Manning, serving as President and COO since January 2023, previously held a managing director role at Rotork, where he oversaw the company’s energy and services divisions. H. Keith Jennings, the incoming CFO, will officially assume his role on January 6th, 2025, succeeding Kurt Wood. Jennings’ addition marks the latest change to Array's executive team. While the extensive experience of the new leadership team is promising, the pace of these transitions raises some concerns—particularly in light of Array’s revenue performance over the past year and the STI write-down. Although their credentials are encouraging, the team’s ability to deliver results remains unproven at this stage.

Management is well incentivized through a balanced compensation structure that includes restricted stock units (RSUs) and performance stock units (PSUs) in addition to their base salary. For more information check out the latest Form DEF 14A.

Board of Directors

The Board of Directors at Array is chaired by Brad Forth, who has an extensive background in the energy industry and is currently a Senior Partner at Neos Partners. Alongside him is Kevin Hostetler, Array's CEO. The board includes seven other directors: Paulo Almirante, Troy Alstead, Orlando Ashford, Jayanthi (Jay) Iyengar, Bilal Khan, Gerrard Schmid, and Tracy Jokinen. Together, they bring expertise in areas such as finance, energy, technology, and corporate governance.

Historical & Recent Performance

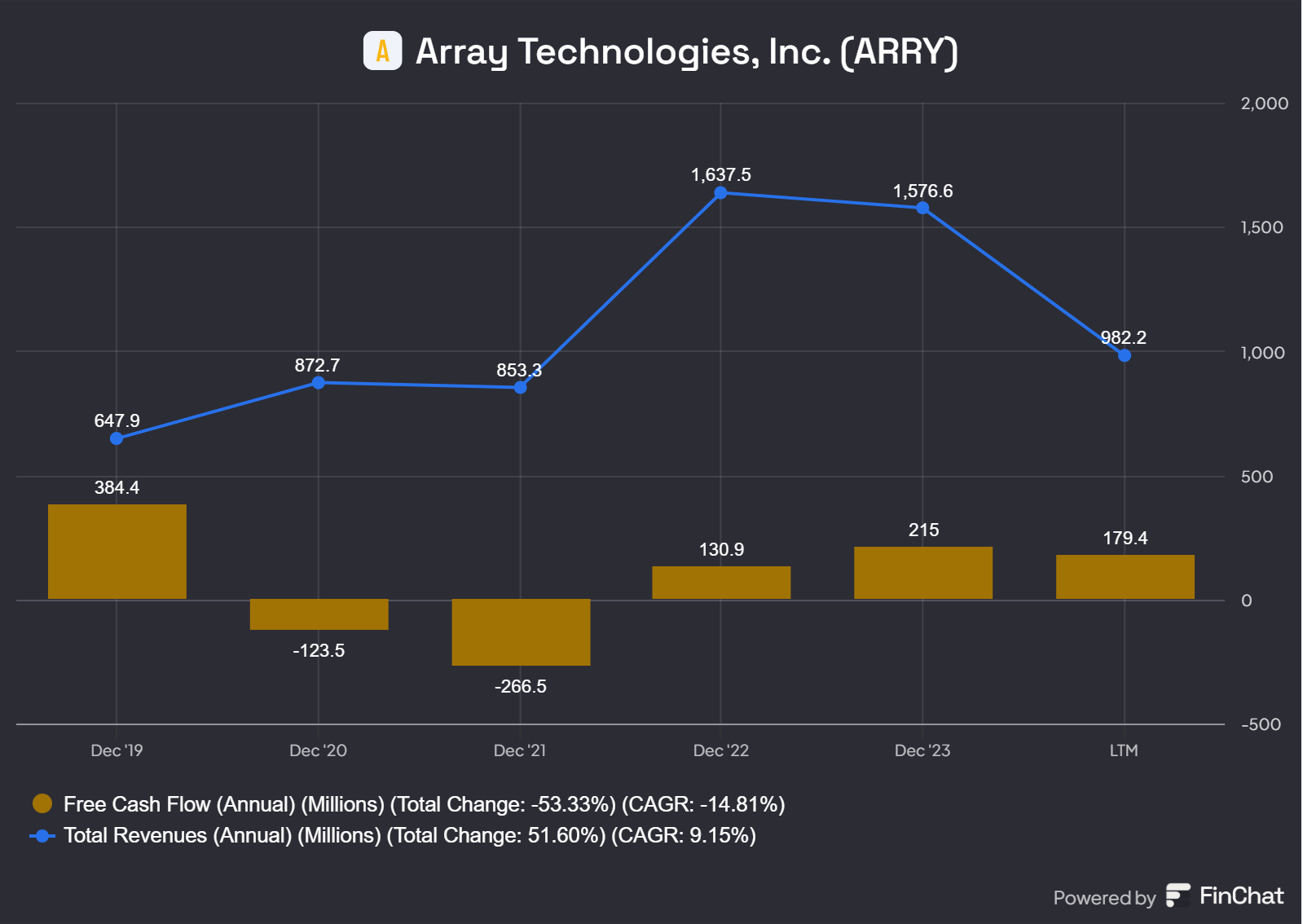

Array experienced steady revenue growth through 2022, followed by a slight decline in 2023 and a more significant drop in 2024. The company attributed this downturn to several factors, including project delays caused by supply chain challenges, permitting and interconnection issues, uncertainty surrounding the Inflation Reduction Act (IRA), and the timing of project financing. However, part of the revenue decline may also reflect a loss of market share to competitors like GameChange Solar and Nextracker, which have pursued more aggressive growth strategies and acquisitions. Additionally, Array’s $162 million write-down related to STI suggests competitive weaknesses and underperformance in certain areas. The company has acknowledged in previous earnings calls that it has been more selective with customers, a strategy that has resulted in ceding some market share. Despite these challenges, Array maintains a strong order book, with a consistently high book-to-bill ratio exceeding 1.5, supported by approximately 80% of Tier 1 customers. Management has reported in their most recent earning call that their win rates on projects are higher than their historical market share. As of Q3 2024, the company reported an order book valued at around $2 billion which is 2x their trailing twelve-month revenues, while its domestic pipeline of opportunities grew to over three times the size of the previous year, indicating strong and sustained demand.

On the profitability front, Array has demonstrated its ability to maintain competitive margins. Gross margins have improved in recent years, driven by the moderation of steel costs, and the company anticipates gross margins in the low 30% range moving forward aided by 45X production credits. Operating margins are expected in the upper teens. Returns on invested capital have fluctuated but seem to moderate in the low teens.

As Array moves into 2025, the company aims to strengthen its sales efforts and capitalize on its market leadership. Array holds a dominant position in the Brazilian market, where it shares the top spot in utility-scale solar and leads the market in distributed generation projects. However, management anticipates persistent challenges in 2025, including permitting and interconnection delays, shortages of high-voltage circuit breakers and transformers, and constraints in EPC (Engineering, Procurement, and Construction) labor availability. Despite these headwinds, there are encouraging signs: lead times for electrical equipment are decreasing, and additional production capacity is expected to come online over the next few years, positioning Array and its customers for improved project execution.

Valuation

Using a variety of valuation methods, including a discounted cashflow model and a reverse discounted cashflow model, I estimate a fair value for Array of around $8.00 per share. As I mentioned prior, I believe that Array is one of those companies where we are best off reverse engineering for our desired outcome and understanding what growth rates and industry factors must play out to achieve this outcome. For instance, assuming modest free cash flow of $100 million, a discount rate of 11%, a 5% annual growth rate over ten years, and 0% terminal value, the resulting present value of free cash flows is approximately $746.08. Adding a rounded down terminal value of $500 million, the total value comes to $1,246.08 million. Dividing this by Array's current shares outstanding of 152 million gives a per-share valuation of approximately $8.19. To put this further into perspective, Array’s fiscal 2023 free cash flow was $215 million.

Given Array’s $2 billion order book, strong number-two market position, consistent book-to-bill ratio over one, and the growing clarity surrounding 45X tax credits, the above free cashflow projections seem quite conservative and that is in spite of the continued headwinds Array faces. Management anticipates double-digit revenue growth through 2025 as they fulfill a substantial portion of their existing order book. I expect the order book to decrease in future quarters due to the accumulation of customer pushouts over the past year. Even so, this growth projection exceeds my current modeling assumptions. Gross margins are forecasted to remain in the low 30s, supported by government incentives. In an optimal operating environment where Array sustains its market share and commodity costs remain near historical levels, a $10 plus share price is likely attainable.

In terms of valuation ratios, Array is currently trading near its historical lows in price-to-sales (P/S). Its price-to-free-cash-flow (P/FCF) is also at historically low levels, translating to an impressive free cash flow (FCF) yield of nearly 22%. When compared to its closest and more profitable peer, Nextracker, Array trades at less than half the multiples for P/S and P/FCF, as well as FCF yield, despite remaining competitive in terms of gross margins and holding a leading market share in some of the markets they compete.

At Array’s current price near $5.60, my fair value estimate of $8 per share would give it a margin of safety of 30%. This translates to an approximate 40% plus upside.

Investment Thesis

Over the past year, Array’s stock price has fallen approximately 70%, and nearly 79% from its 2023 high of around $26. This sharp decline reflects growing investor pessimism driven by several factors, including project delays and pushouts caused by supply chain disruptions and financing challenges, currency weakness in Brazil, heightened competition, and analyst downgrades. Compounding these issues, the company reported a $162 million goodwill write-off related to the STI acquisition, further eroding market confidence. Broader weakness across the solar sector has also weighed heavily on the stock, amplifying its decline.

Despite these misfortunes, Array is well positioned for price appreciation at its current levels. Array is expected to bear the fruits of its large orderbook consisting of approximately 80% tier 1 customers over the next year. Their book-to-bill ratio and project win rates have remained strong in face of a down solar sector, and the company has proven itself capable of competing with major players in the industry, namely Nextracker. In October, the U.S. Department of Treasury issued its final rules on the 45X credits. This development has provided much needed clarity surrounding project costs in the U.S. domestic market, and gives manufacturers, customers, and financiers greater confidence in their planning. This will likely increase the demand for solar projects.

Taking a more sectoral view, the solar industry, particularly in areas of utility scale projects, are expected to continue growing in the coming years to support the world’s ever-increasing demand for electricity. Increased adoption of technologies, data centers, EV infrastructure, cryptocurrency, urbanization, population growth, infrastructure expansion, and overall economic growth will create a steady demand for electricity for years to come. In addition, demand for renewable energy solution and government policies related to decreasing emissions will provide additional push for solar. Solar energy has accounted for more than 50% of new electricity-generating capacity being added to the grid since 2023. This is a trend I intend to monitor. The continued decline in solar panel costs, coupled with technological advancements like the adoption of bifacial panels and improvements in energy storage, is expected to enhance the viability of utility scale solar projects. This will likely drive demand for solar tracker systems and advanced software solutions that optimize efficiency and safeguard solar arrays against adverse weather conditions. Additionally, as solar energy becomes increasingly viable, projects on challenging and uneven terrain are anticipated to become more common, creating a growing need for innovative solutions such as Array’s OmniTrack system.

Some of the pessimism surrounding the industry stems from concerns about potential changes to energy policy under the Trump administration. However, I believe it is unlikely that the new administration will roll back the government incentives that have been driving the growth of the solar industry. The administration is expected to pursue a policy agenda aimed at “unleashing American energy,” promoting energy independence, resilience, and increasing energy exports. If policy changes do occur, they will likely focus on boosting domestic energy production rather than directly targeting solar incentives. The area of potential risk, in my view, lies in the anticipated rollback of regulations, which could reduce overall energy and electricity costs over time. This, in turn, might diminish the economic appeal of solar projects. Furthermore, many key government incentives, including the 45X credit are not scheduled to begin phasing out until 2030 which provides a solid growth runway until then. Refer to the following CNBC article for more discussion in this area.

Array is challenging to value due to its inconsistent cash flows and sensitivity to market dynamics, which make long-term projections beyond a few years highly uncertain. The company lacks the consistent returns on invested capital and durable competitive advantages that I typically prioritize in an investment. For these reasons, I have taken a highly conservative approach in my valuation methods. At its current price near $5.60 a share, Array trades at a modest discount based on my free cash flow projections and relative to its closest peer, which itself is trading at the lower end of its historical valuation range. For the reasons I laid out above and in previous paragraphs, I believe Array is well positioned to appreciate in value and grow from its current levels. Array is not a company I plan to hold for the long term. I intend to sell the majority of my position upon realizing my fair value estimates, and assuming no significant changes to the company’s fundamentals or operating environment.

Thanks for reading and wishing you a sunny day!

8/19/25 – Position Closed: +113.4% pretax return on $4.23 cost basis.

Not bad for 8 months. Utility-scale solar remains one of the fastest ways to bring new energy on-grid to meet accelerating AI and industrial demand. Clarity on tax incentives led to recent price appreciation narrowing the risk/reward profile. Simply put, I believe there are higher-quality businesses to place capital today. Also sold as part of a strategic shift away from companies with elevated default risk under potential austerity conditions.

Really apreciate the depth here on ARRY. The centralized motor architcture point is interesting, havent thought much about how that single motor controlling 32 linked rows vs competitors needing one per row would impact maintennance costs over a 30 year lifecycle. The STI writedown is concerning though. Do you think their conservative approach on customer selectivity is the right move given the market share losses, or should they be more aggressive to compete with Nextracker? Curious if the Swap Robotics investment pays off beyond just vegetation management too.