Atkore Inc. Deep Dive & Valuation ($ATKR)

Atkore is a manufacturer of electrical raceway systems and mechanical products that support infrastructure, industrial, and construction markets, well positioned to benefit from secular demand trends.

Atkore Inc. is a leading manufacturer of electrical and infrastructure-related products, serving the construction and industrial sectors. The company provides a broad portfolio of products for electrical power systems, including conduits, cables, and installation accessories. Atkore also offers infrastructure solutions such as metal framing, mechanical pipes, perimeter security systems, and cable management solutions, ensuring the protection and reliability of critical infrastructure. For many of its product categories, Atkore holds the #1 or #2 market position in the United States by net sales. The company is expected to experience steady demand over the coming decade, driven by trends in electrification, infrastructure development, and data centers.

Atkore's history began in 1959 in Blue Island, Illinois, when Allied Tube & Conduit patented and introduced the "Flo-coat" galvanization process. Starting with a single tube mill and 10 employees in 1960, the company moved to Harvey, IL, by 1965, growing to 100 employees. Over the next two decades, Allied pioneered innovations like IMC, an alternative to rigid conduit and expanded through acquisitions. In 1987, Allied was acquired by Tyco Laboratories, later called Tyco International. Several years of poorly managed acquisitions and internal corruption would lead to Tyco International selling a majority stake of its electrical and metal products business to private equity firm Clayton Dubilier & Rice, LLC in 2010, forming Atkore Inc. as a standalone company. Atkore would go on to make several acquisitions of its own, expanding its product portfolio in areas of fire suppression systems, PVC, plumbing and more. In 2014, Atkore would repurchase Tyco’s remaining stake in the company. Atkore Inc. went public in 2016 on the NYSE under the ticker ATKR.

Today, Atkore Inc. is headquartered in Harvey, IL. They employ approximately 5600 full time employees across six international locations including Australia, Belgium, Canada, China, New Zealand, and the U.K. Atkore manufactures products in 49 facilities and operates a total footprint of approximately 7.5 million square feet of manufacturing and distribution space in eight countries.

Operations:

Atkore Inc. derives its revenues from the design, manufacturing, and sale of electrical and infrastructure components. The company reports revenues in two segments: Electrical, and Safety and Infrastructure.

Electrical consists of four subcategories that cover Metal Electric Conduit and Fittings, Plastic Pipe Conduit and Fittings, Electrical Cable and Flexible Conduit, and Other Electrical Products such as international cable management, fiberglass conduit and corrosion resistant conduit.

Safety and Infrastructure consists of two subcategories including Mechanical Tube, and Other Safety and Infrastructure Products such as metal framing and fittings, construction services, perimeter security and cable management. For a full understanding of their product offering check out their products and services page. As part of the Safety and Infrastructure segment, Atkore offers construction services with their own in-house design and engineering teams, construction teams, and prefabricated products.

Manufacturing, Materials, & Distribution

Atkore manufactures its products across 49 facilities in eight countries and utilizes additional warehousing and distribution locations, many of which are leased. Most of these leases are operating leases with an average remaining term of 9.5 years. The company strategically positions its manufacturing, distribution, and assembly centers to maximize route efficiency, enhance market coverage, and minimize costs.

Atkore is most recognized for its competitive tube and conduit products. The company believes itself a leader in the in-line galvanizing manufacturing process. Using specialized equipment and manufacturing methods Atkore is able to produce a variety of low cost and high-quality galvanized tube products.

“For example, our subsidiary, Allied Tube & Conduit Corporation, or “Allied Tube,” developed an in-line galvanizing technique (Flo-Coat) in which zinc is applied in a continuous process when the tube and pipe are formed. The Flo-Coat galvanizing process provides superior zinc coverage of fabricated metal products for rust prevention and lower cost manufacturing than traditional hot-dip galvanizing. Another example is our Cellular Core conduit, which employs a coextrusion process to create three firmly bonded layers with the inner layer as a cellular core, creating a conduit that weighs less and is more flexible while meeting UL standards.”

In the course of manufacturing, Atkore uses a variety of raw materials including steel, copper, polyvinyl chloride resin used in PVC, and HDPE resign. Zinc and aluminum are also used in their manufacturing. Atkore maintains a diverse supply base to mitigate disruptions in raw material availability. Its primary steel suppliers include Cleveland-Cliffs, Steel Dynamics, and Nucor, while copper is sourced from AmRod, SDI LaFarga, and Nexans. For PVC, the company relies on Westlake, Formosa, and Oxy Vinyls, and for HDPE resin, suppliers include LyondellBasell and Baystar. Atkore’s operations may be impacted by fluctuations in commodity prices. Historically the company has not engaged in hedging activities.

Atkore distributes its products through a network of electrical, industrial, and specialty distributors, as well as original equipment manufacturers (OEMs). Products are shipped from Atkore's four regional distribution centers, manufacturing centers, along with over 38 dedicated facilities operated by their agents. The majority of distribution is concentrated in North America, with additional locations in Australia, New Zealand, and the U.K. In 2023, distribution-based sales contributed approximately 83% of the company’s net sales. Atkore primarily relies on third-party logistics providers for product distribution but also maintains its own dedicated carrier fleet to ensure priority and expedited deliveries for key customers. The company has invested significantly in technology, offering customers streamlined ordering and invoicing processes, along with enhanced transparency and real-time tracking of orders.

Customers

Atkore’s customers primarily consist of electrical, industrial and specialty distributors, who sell to contractors, and OEMs. These customers are typically serving industries in areas of commercial and residential construction, infrastructure, energy, data centers, telecom, industrial manufacturing, water and gas, transportation and more. Customers in sectors such as infrastructure, renewable energy systems, data centers, warehouses, and electric vehicle (EV) charging stations have been significant drivers of demand and are expected to continue driving growth over the next decade.

Atkore’s customers include both regional and global distributors, industrial distributors as well as big box retailers. Major customers include Consolidated Electrical Distributors, Graybar Electric Company, Rexel, Sonepar S.A., U.S. Electrical Services, Wesco International, Crescent Electric Supply Co., and United Electric Supply Company, Affiliated Distributors, IMARK Group, and STAFDA. In fiscal 2023, Atkore’s top ten customers accounted for 38% of total sales, consistent with previous years, with Sonepar USA alone contributing over 10% of sales. Historically, approximately 90% of sales have come from U.S. based customers.

Industry Overview & Outlook:

Atkore serves the electrical and infrastructure industries. Demand for their products is influenced by the demand within their end markets including both residential and non-residential construction, renovation, and infrastructure projects. Nonresidential construction accounts for a significant portion of business.

The demand for Atkore’s products is influenced by several key factors related to the industries in which it operates. Construction activity plays a significant role, with both commercial and residential development driving demand for electrical raceways, conduits, and cable management products. Additionally, large-scale infrastructure projects, such as highways, airports, and energy grid expansions, further increase the need for Atkore’s mechanical and perimeter security solutions. Economic conditions are another critical driver; when the economy is growing, businesses are more likely to invest in new construction and infrastructure, whereas economic downturns can reduce such spending and negatively impact demand. The American Institute of Architects (AIA) is an excellent resource for up-to-date information on business conditions and forecasts in the non-residential construction industry.

Government policies and regulations also heavily affect the industry. Infrastructure spending programs and changes to building codes or safety standards can create new opportunities for growth by requiring updated electrical and mechanical products in construction projects. Technological advancements, particularly in the areas of data center expansion, renewable energy, and the electrification of transportation, have increased the need for robust electrical infrastructure, further driving demand for Atkore’s solutions. Meanwhile, supply chain dynamics, such as the availability and cost of raw materials like steel, aluminum, and copper, influence both production costs and pricing. Efficient logistics and shipping also affect how quickly the company can meet demand in various markets.

Energy and utility sector investments, especially in modernizing aging power grids and improving energy efficiency, create additional demand for Atkore’s products used in electrical and mechanical systems. Urbanization and population growth spur the need for new commercial buildings, housing, and infrastructure, all of which rely on the company's products to meet electrical and mechanical needs. Atkore is expected to be a downstream beneficiary of the BEADs act, although when that money finally gets dispensed by the government remains unknown. Finally, sustainability trends are becoming increasingly important, with green building initiatives and stricter environmental regulations pushing for more eco-friendly solutions. This growing focus on sustainability is likely to continue shaping demand for products in the construction and infrastructure industries.

For a near-term outlook, the industry often refer to resources such as The Architectural Billing Index and The Dodge Momentum Index to gauge market trends. These indexes provide insights into construction activity and project planning, which are leading indicators of demand for Atkore's products. Typically, changes in these indexes precede shifts in Atkore’s business by approximately six to twelve months, as construction projects progress from planning and design to the actual procurement of materials, driving the demand for electrical and infrastructure products. This lag allows the company to anticipate market conditions and adjust operations accordingly.

In a 2024 Oppenheimer industry growth conference, Atkore identifies a few other key metrics that the company watches in forecasting demand and pricing. The fist is the Association of Builders and Contractors (ABC) and their Construction Backlog Indicator which reflect the amount of work expected to be performed by commercial and industrial construction contractors in the coming months. In the August report the Construction Backlog Indicator scored 8.2 months, although suggested lower construction industry confidence and declining profit margins. Another metric that Atkore monitors is the employment levels for non-residential construction. For this information check out FRED’s All Employees, Nonresidential Building Construction data or again check out the ABC site for a more comprehensive industry breakdown.

Growth Outlook

Based on the above information and industry trends, I would say that Atkore’s growth prospects are promising and likely to grow steadily moving forward. I place the company’s revenue growth rate at a modest 4.5% and refrain from speculating on the growth rates of the various industries it serves or emerging trends, believing its current valuation provides a level of safety. Notably, recent revenue declines have been driven more by a decrease in average selling prices rather than a drop in sales volume, indicating that demand remains robust. As interest rates begin to ease, I anticipate that Atkore will benefit from increased investment in construction, infrastructure, and renewable energy projects, supported by more accommodative monetary policies, which should further drive demand for its products.

Analyzing trends across several of Atkore’s key product lines, including electrical conduit, PVC conduit, PVC pipe, flexible electric conduit, mechanical pipe, and cable trays, reveals growth rates ranging from mid to high single digits.

Regulations

Atkore operates in industries that are subject to a variety of regulations, particularly in the areas of safety, environmental compliance, and product standards. These regulations include strict building and electrical codes, such as the National Electrical Code (NEC) in the United States, which governs the installation and use of electrical products like conduits and fittings. The company must also comply with OSHA (Occupational Safety and Health Administration) guidelines, ensuring that its products meet workplace safety standards. Additionally, environmental regulations such as those enforced by the EPA (Environmental Protection Agency) require Atkore to manage the environmental impact of its manufacturing processes, including emissions control, waste management, and material sourcing, especially for PVC and steel products. Such is the case at their Wayne County plant in my home state of Michigan. International markets add layers of complexity, with Atkore needing to comply with regional and country-specific standards.

Competitors

The majority of Atkore’s sales takes place in the United States. Domestic competitors range from national manufacturers to smaller regional manufacturers and differ by product lines. The company also faces competition from manufacturers in Canada, Mexico, Columbia, The Dominican Republic, China, and other international markets who are increasing their imports to the Unites States. There is limited differentiation in products between competitors leaving them to compete on the basis of product offering, product innovation, quality, service and price. In their 2023 10K, Atkore states “We believe our customers purchase from us because we provide value through the quality of our products, the breadth of our portfolio and the timeliness of our delivery.”

Atkore’s main competition by segment include:

Electrical: Zekelman Industries, Inc., Mitsubishi Corporation, Nucor Corporation, Southwire Company, Dura-Line Corporation, and Encore Wire Corporation (acquired by Prysmian).

Safety & Infrastructure: Zekelman Industries, Eaton Corporation, ABB Ltd., Hubbell Incorporated, nVent Electric, and Haydon Corporation.

Other competition and industry peers include Acuity Brands, AZZ Inc., Beldon Inc., Cornerstone Building Brands, Littlefuse Inc., Schneider Electric, and Valmont Industries.

Acquisitions:

A key component to Atkore’s growth strategy has been acquisitions. The company has consistently been on the hunt for bolt-on and synergistic style acquisitions that strengthen, expand, and diversify their product portfolio. Some of their notable acquisition over the past few years have included:

Elite Polymer Solutions (November 2022): Atkore acquired this Texas-based company, which manufactures HDPE conduit. This acquisition strengthened Atkore’s presence in the telecommunications, utility, and transportation markets, enhancing HDPE product offerings.

United Poly Systems (June 2022): This acquisition expanded Atkore’s manufacturing capacity for HDPE pipe and conduit, a market benefiting from U.S. infrastructure investments. United Poly Systems has operations in Missouri and New Mexico, helping Atkore serve growing demand from infrastructure projects.

Cascade Poly Pipe and Northwest Polymers (August 2022): These two Oregon-based companies were acquired together, furthering Atkore’s presence in the HDPE conduit and recycling markets.

Talon Products (May 2022): Atkore acquired Talon Products, which specializes in non-metallic, injection-molded components. This acquisition helped Atkore diversify its product range in the electrical sector.

Four Star Industries (December 2021): Atkore added this HDPE conduit manufacturer to bolster its offerings in the telecommunications and infrastructure markets. This acquisition positioned Atkore to better serve industries like broadband and renewable energy, aligning with nationwide infrastructure investments.

Other acquisitions over the years have included Sasco Tubes & Roll Forming Inc., FRE Composites, and Queen City Plastics. For a complete timeline of Atkore’s acquisitions check out the M&A link on their website. Many of the listed acquisitions have been acquired through cash on hand.

Competitive Advantages:

In my research and analysis of Atkore, I believe the company does benefit from a few competitive advantages despite the highly competitive environment. Atkore’s competitive advantages include:

Economies of Scale: Atkore holds the #1 and #2 market positions in the majority of its product lines across the United States. This dominance allows the company to achieve lower production costs per unit by leveraging higher volumes and efficiently spreading fixed costs. This cost advantage strengthens its pricing power and competitive position.

Supply Chain and Distribution Efficiency: Atkore takes great pride in its highly efficient supply chain, which includes advanced distribution centers, technical applications, and fast delivery options. Their distribution centers stock the entire Atkore product line, creating a one-stop-shop for customers. The company's “one order, one delivery, one invoice” system simplifies the purchasing process, while flexible freight minimums help customers save money. These initiatives not only streamline operations but also enhance customer loyalty and satisfaction by reducing friction in the procurement process. Competitors have not been able to repeat this.

Manufacturing Capabilities: Atkore’s superior manufacturing processes provide a significant edge over competitors. One standout process is the patented in-line galvanizing Flo-Coat technique used on pipe and tube products, which applies a zinc coating that prevents rust and corrosion, and extends the life of the product while providing a simplified solution for customers. This method can be used on a broad range of Atkore products and is significantly cheaper than the hot-dip galvanizing or other corrosion resistance processes used by competitors. Additionally, Atkore warranties these products, which improves customer loyalty and makes them a preferred solution.

Another notable manufacturing capability is Atkore’s coextrusion process for conduit products creates a conduit with three bonded layers, including a cellular core, resulting in a product that is lighter, more flexible, and meets UL standards. This innovative manufacturing further differentiates Atkore in the marketplace. I will note that I do not believe these manufacturing capabilities to be durable competitive advantages, as competitors may always come up with their own improved method.

Management:

Atkore’s Management team consists of 12 members. For the sake of time I will not cover all of the, but for a full overview refer to their Management Page. Atkore’s President and CEO is William E. Waltz. Waltz has been CEO since 2019 and served Atkore in several other executive roles since joining the company in 2013. Waltz sits on Atkore’s board of directors and is also a Governor of the National Electrical Manufacturing Association (NEMA). Atkore’s CFO is John Deitzer. Deitzer is fresh to the CFO role, promoted to the position in August of 2024. Prior he served as VP of investor relations at Atkore. I believe that Atkore has a strong management team and has demonstrated strong capital allocation ability with respect to share repurchases and acquisitions. Executive pay consists of a competitive base pay and performance-based equity awards in the form of stock options, RSUs, and PSUs. I believe that management is well incentivized with their current compensation package.

Atkore’s Board of Directors consists of 9 members. The Chairman of the Board is Michael Schrock, who has held the position since 2018. “Mr. Schrock brings more than forty years of experience in the electrical industry and more than a dozen years of experience on public company boards.” For details on the other board members, please refer to Atkore’s Board of Director page. Board members are compensated through fees earned and are awarded $140,000 in stock, delivered in the form of Restricted Stock Units (RSUs), aligning their interests with the long-term performance of the company.

Capital Allocation:

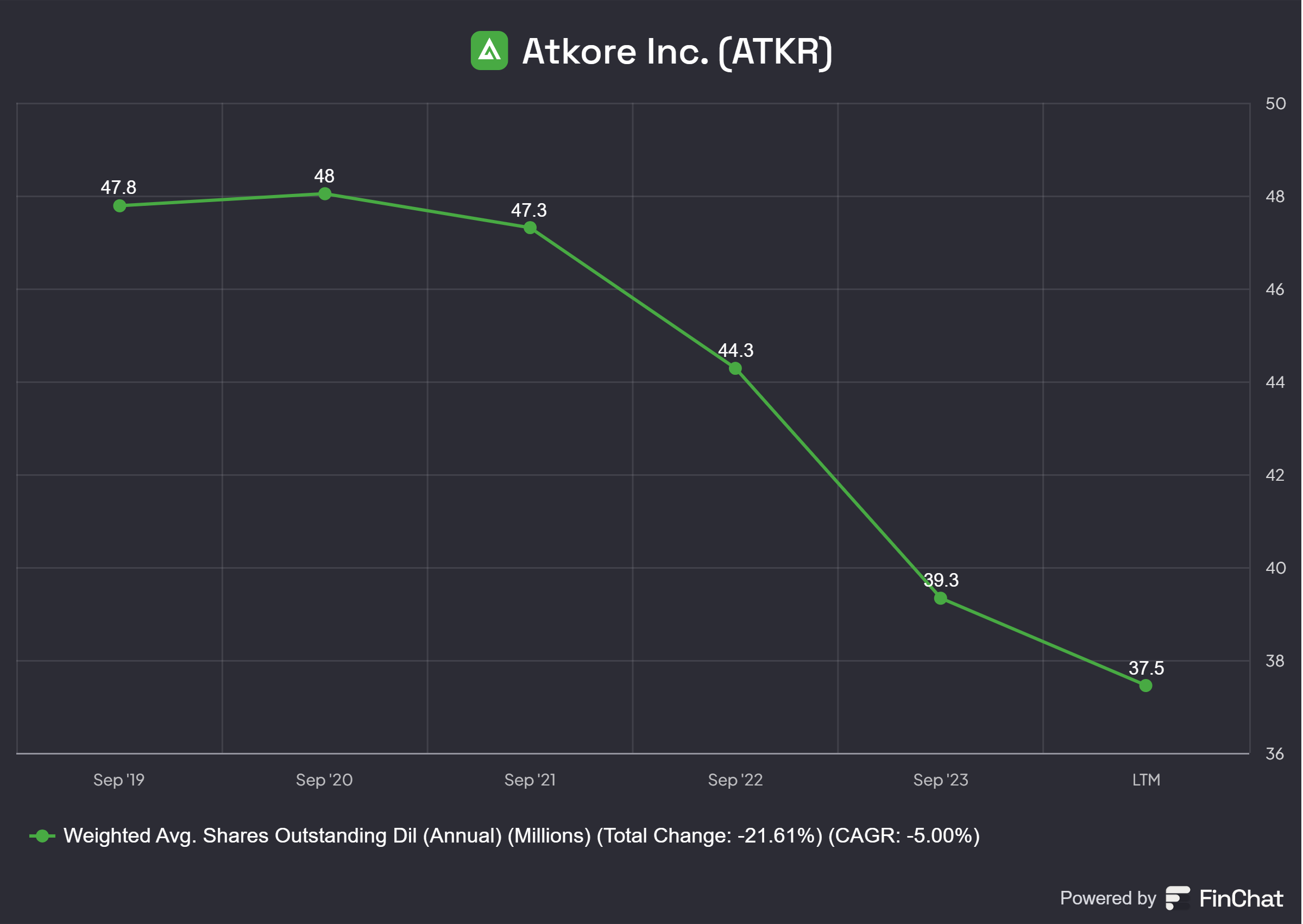

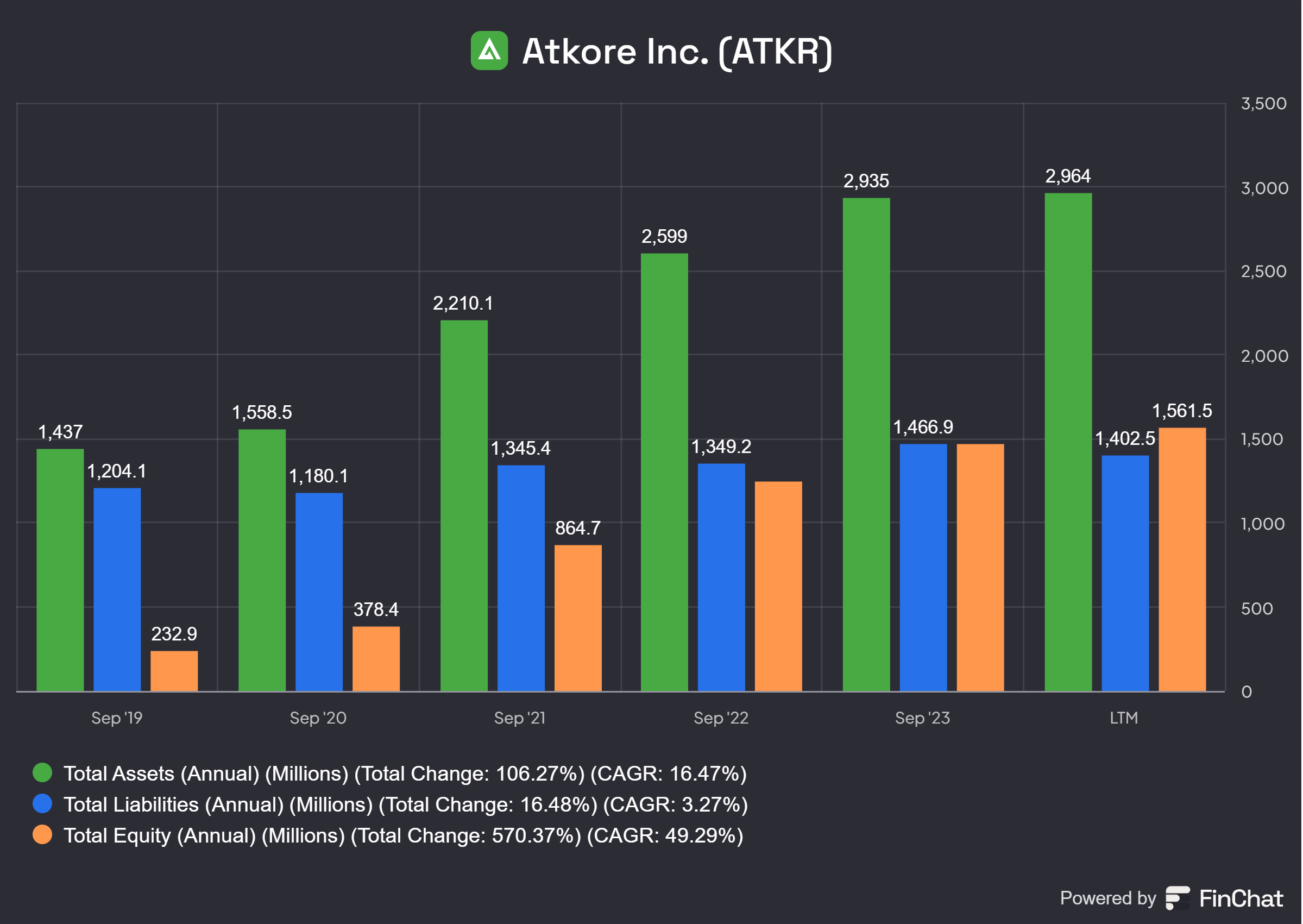

Historically, Atkore’s capital allocation strategy has focused on share repurchases, debt repayments, acquisitions, organic investments, and, beginning in 2024, the introduction of a quarterly dividend. In 2023, the company repurchased approximately 2.4 million shares valued at $491 million, and this continued into 2024 with an additional 1.45 million shares repurchased as of the Q3 earnings report. Atkore has repurchased 42% of their shares outstanding since going public in 2016. As of July 31, 2024, Atkore had 35.86 million shares outstanding.

The company carries $764.3 million in long-term debt, consisting of $400 million in senior notes due 2031 with an interest rate of 4.25%, and $371.9 million in a senior secured loan due 2028, with interest rates ranging from 5.6% to 7.7%. Given Atkore’s strong financial performance, the company is expected to meet these obligations without issue. In terms of organic investments, Atkore has expanded its Indiana facility and distribution centers to support growth. Additionally, in November 2023, the company announced its first-ever quarterly dividend of $0.32 per share, opening up another channel for returning capital to shareholders.

Risks:

Atkore’s business is subject to several risks. Below are some that I believe to be most relevant.

Business Conditions: Atkore's performance is closely tied to general economic conditions and specific trends in its key end markets, such as non-residential and residential construction, renovations, OEMs, and international markets. Any downturns or disruptions in these sectors—whether due to economic recessions, rising interest rates, tighter credit markets, or the withdrawal of federal funding may negatively affect demand for Atkore's products. Non-residential construction, a large portion of Atkore’s business, is particularly vulnerable to cyclical downturns, and any declines in this area would have a significant adverse impact.

Commodity Risks: Atkore is highly dependent on key commodities, including copper, steel, polyvinyl chloride (PVC) resin, zinc, and aluminum, which are essential for many of its product lines. Price fluctuations in these commodities could result in higher input costs that the company may not always be able to pass on to customers. The inability to secure materials at reasonable prices or manage price volatility could negatively affect Atkore’s profitability.

Competition: The industry has seen a great deal of consolidation over the past decade which has resulted in improved margins across the industry as a result of economies of scale and decreased competition. However, as of recent there have been increased competition from foreign imports, especially Mexico. Atkore’s ability to respond to competition and maintain competitive product offerings and customer loyalty are important to maintaining market share. I believe that the U.S. government will eventually take action to protect American companies especially in the case of a tentative Trump Administration.

Customer Concentration: In fiscal 2023, Atkore’s ten largest customers accounted for approximately 38% net sales. The loss of a major customer or the inability of a major customer to pay would have a material impact on Atkore’s revenues.

Other Risks: Other risks may include rising freight costs and potential disruptions in IT systems, including cybersecurity threats, which could lead to significant operational challenges. Changes in trade policies, adverse weather events, and evolving environmental and health and safety regulations may affect manufacturing capabilities or create new liabilities for the company. Atkore also faces labor-related risks, such as the presence of labor unions, difficulties in attracting skilled workers, and potential labor shortages in both its operations and its key end markets. Furthermore, the company’s international exposure introduces risks related to geopolitical instability, currency fluctuations, and compliance with foreign regulations, all of which could affect its global operations.

Historical and Recent Performance:

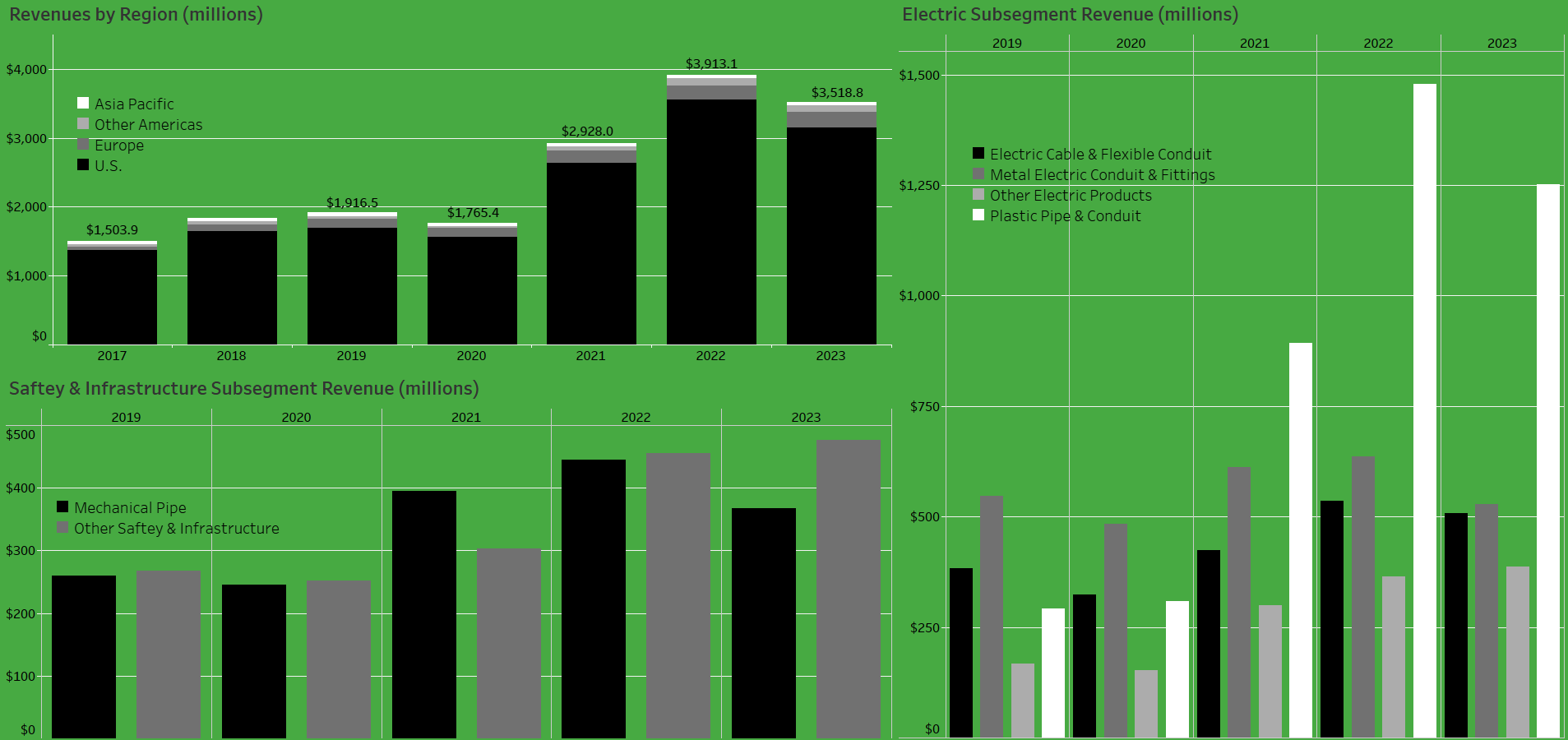

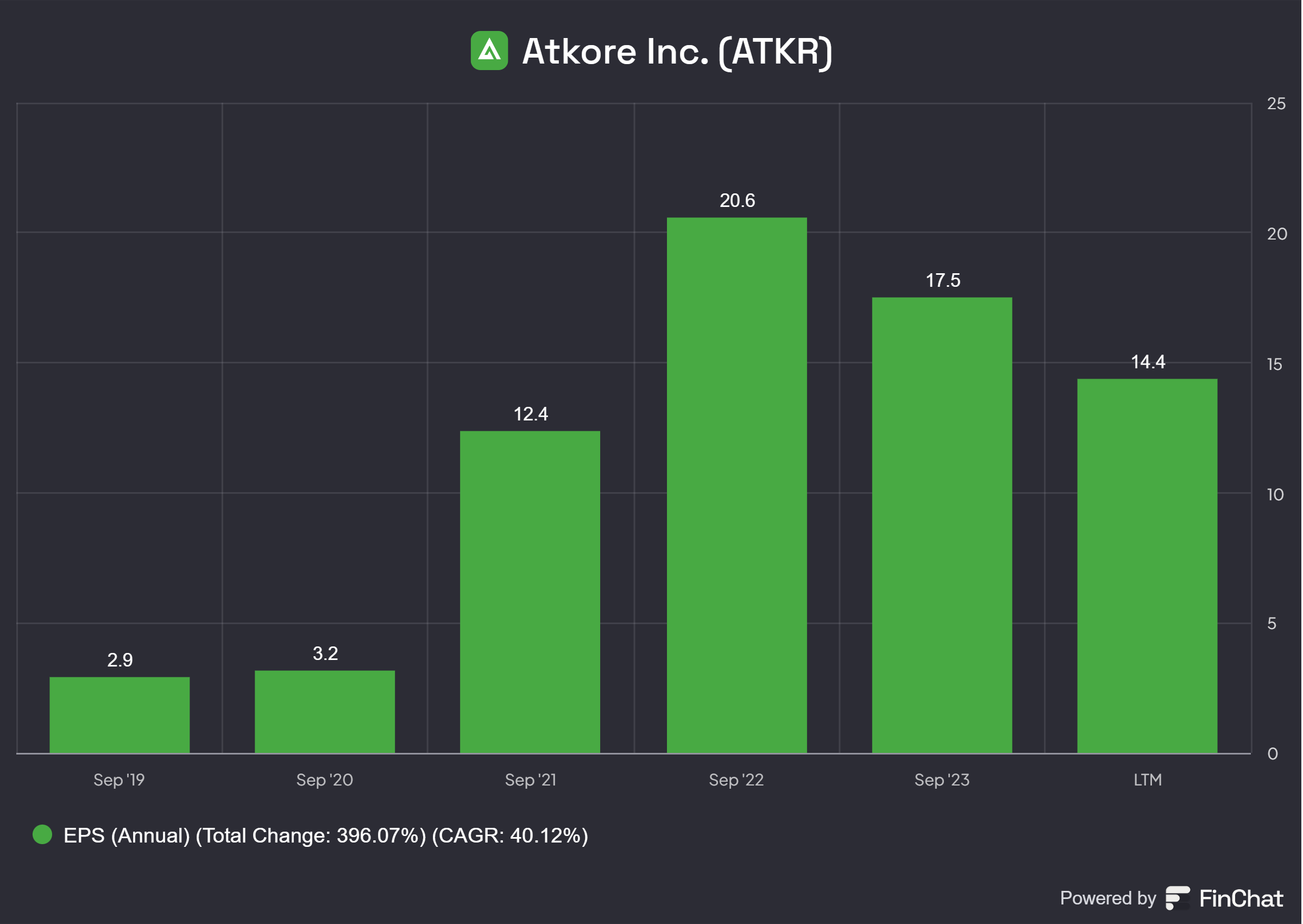

Since 2016, Atkore has achieved a compound annual growth rate (CAGR) of 12.7% in its revenues. In 2023, revenue reached $3,518.8 million, down from its peak of $3913.9 million in fiscal 2022. It is anticipated that revenues will normalize throughout the remainder of the year due to ongoing price moderation, which is expected to further normalize profit margins. Over the same period, EPS has achieved a CAGR of 51.6%. Current EPS sits around $14.4 as a result of lower net income. Atkore’s share price peaked in April of 2024 at around $195. Over the past six months, the stock has declined by more than 50% due to a weaker than expected commercial construction market. This downturn was compounded by management's revision of earnings guidance downward from $17 to $14.4, along with growing concerns regarding competition from foreign imports.

Atkore's most rapidly expanding product line over the past three years has been its plastic pipe and conduit, which is extensively utilized in the utility and residential sectors. The second-largest subsegment comprises metal and electrical conduit and fittings, which is predominantly employed in commercial markets and data centers.

Over the past decade, Atkore has seen a steady increase in margins, largely due to industry consolidation. However, recent trends indicate a decline in margins from the levels seen during Covid-19 in 2021 through 2022, attributed to price moderation. For my financial modeling, I have assumed an operating margin of approximately 17%.

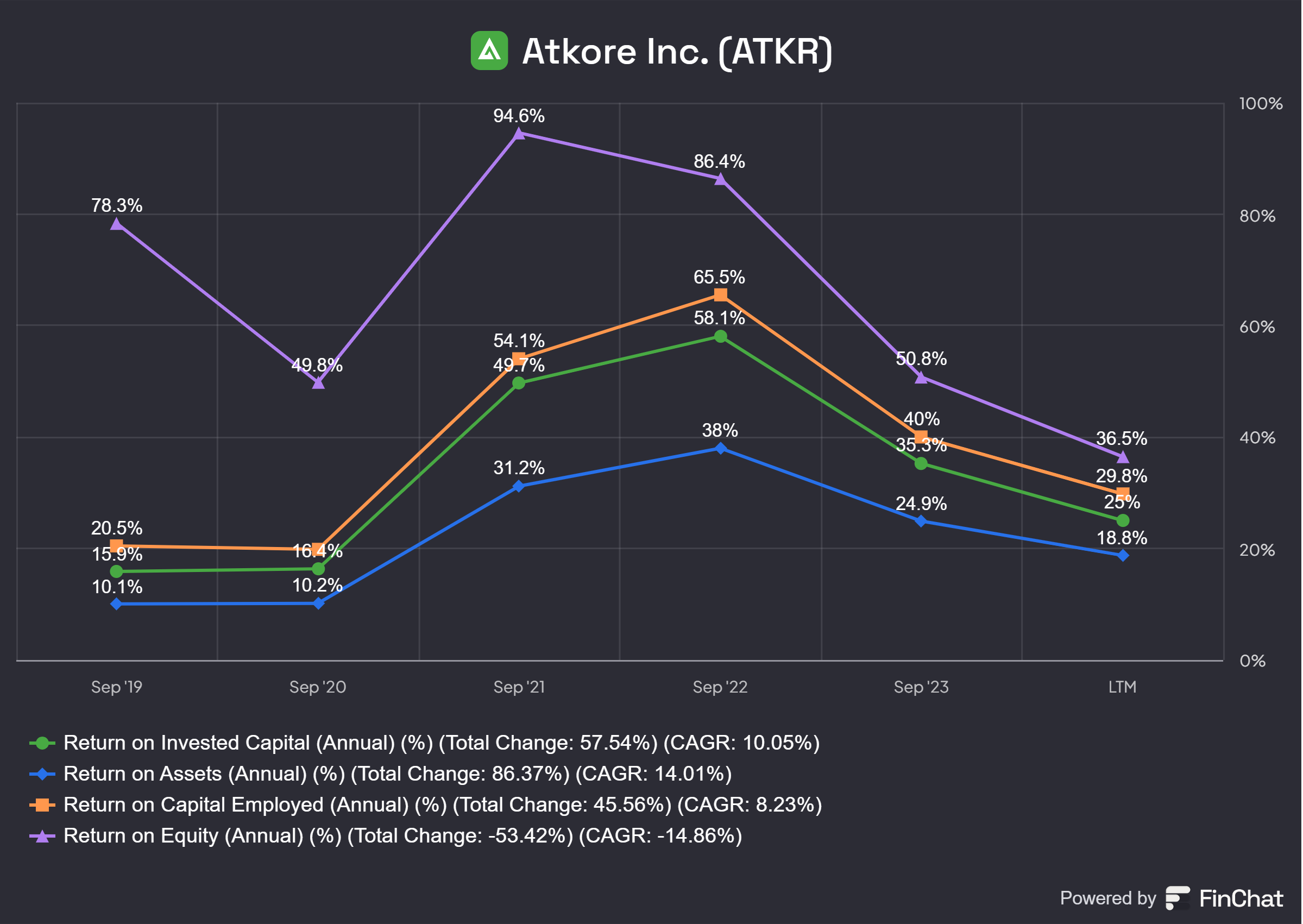

Examining capital efficiency, Atkore has consistently achieved a return on invested capital (ROIC) exceeding 15% over the past five years. Compared to peers and other companies within the electrical equipment industry, Atkore has consistently shown superior returns.

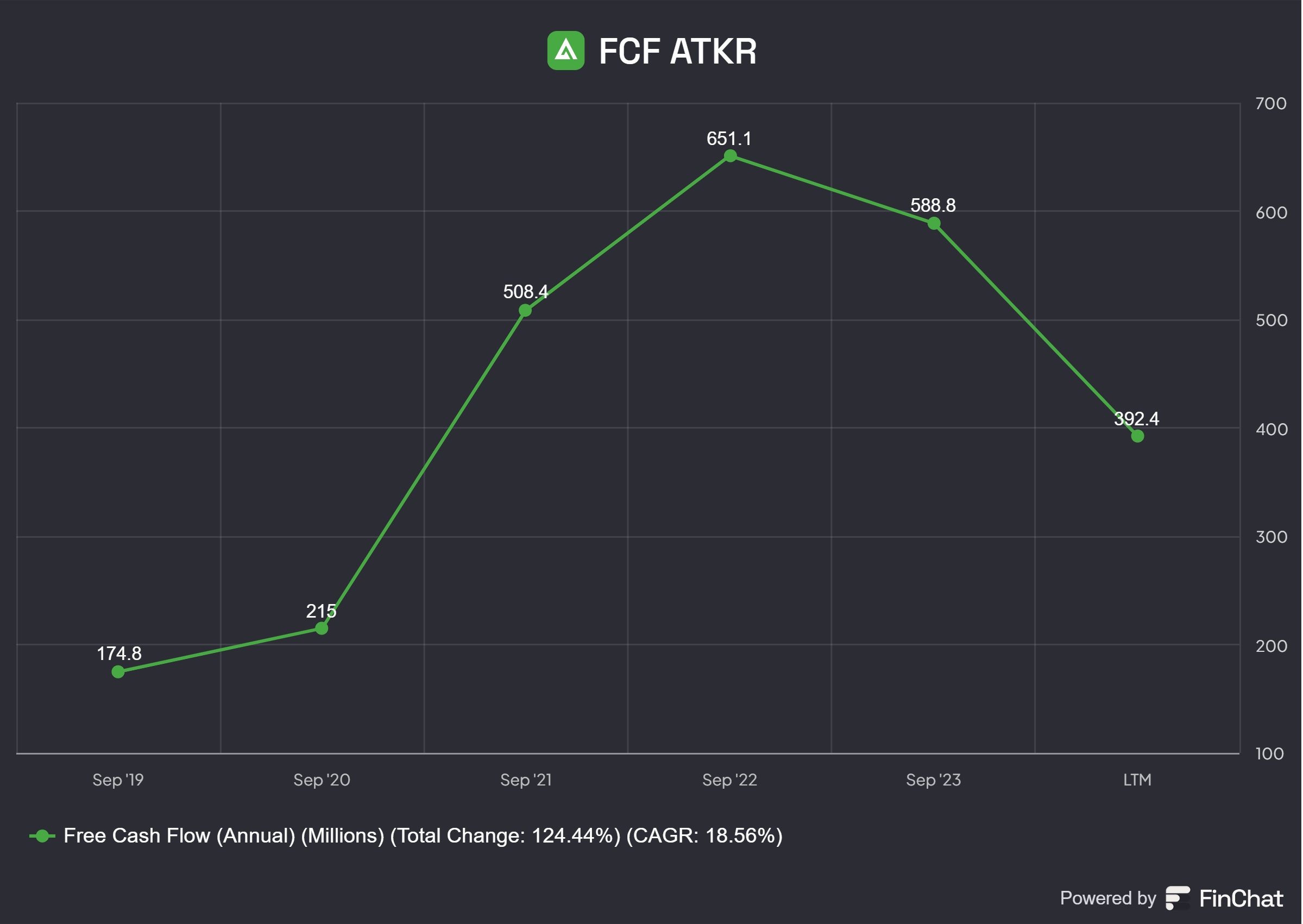

Free cash flow has seen a similar story as revenues and earnings. I project Atkore’s free cash flow to end the year in the $325 to $350 million before stabilizing and resuming a growth trajectory fueled by secular demand for electrical industry products.

Heading into 2025, management expects growth initiatives in key areas such as solar, HDPE, water, and construction, along with continued enhancements to their regional service centers, to drive positive year-over-year performance. They project low single-digit volume growth across many product lines, supported by a more favorable interest rate environment. However, management remains cautious about the pricing landscape. Historically, Atkore's leadership has maintained a conservative approach, often under-promising and over-delivering, as evidenced by their track record of earnings beats. Given the challenges in the commercial construction sector this past year and recent management changes, it appears the company is exercising heightened caution in its guidance.

Valuation

Using a both a regular and reverse discounted cash flow model I estimated a fair value for Atkore at around $125 a share. I believe this to be a conservative estimate using a variable revenue growth rate starting at 4.5% and declining to 3% on $3150 million of revenues, a normalized operating margin at 17%, tax rate of 22%, ROIC of 20%, and a discount rate of 11%. At Atkore’s current price in the mid $80s my fair value estimate would give it a margin of safety of 30%. This would give Atkore a roughly 45% upside.

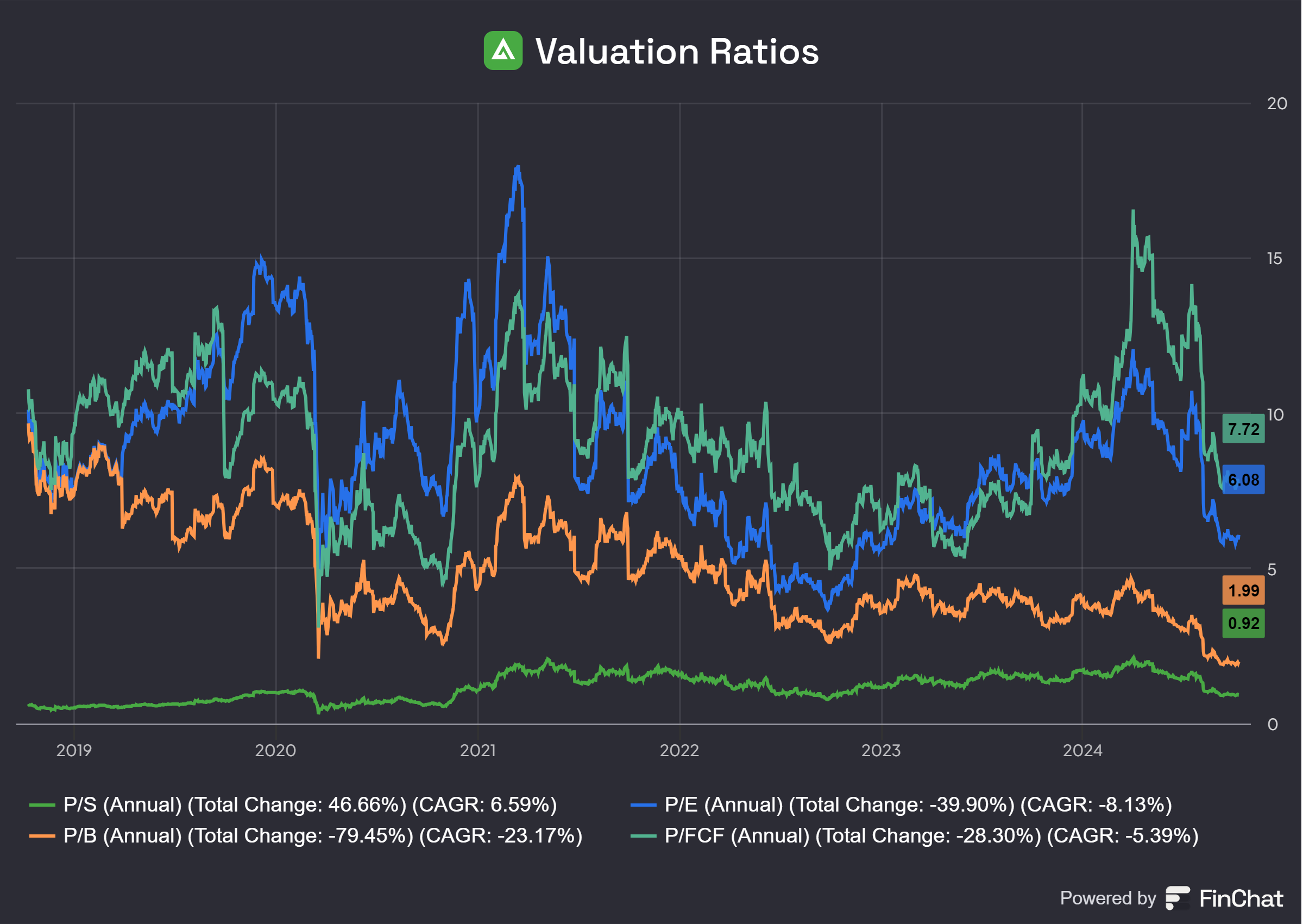

With respect to valuation ratios Atkore currently trades at or near the historical low ends of its price to book, price to sales, price to earnings, and price to free cash flow.

Final Thoughts

Atkore is well positions to benefit from secular trends in the electrical infrastructure space. The growing demand for electrification, data centers, renewable energy, electric vehicle charging stations, digital infrastructure upgrades, and telecom is expected to drive consistent, long-term growth for Atkore's products. The company benefits from both manufacturing and supply chain distribution advantages that are difficult for competitors to duplicate and increase customer satisfaction. Additionally, Atkore benefits from a level of economies of scale offering several top selling product lines that make them a preferred pick among customers. The company has demonstrated a solid track record of capital allocation especially in areas of acquisitions and share repurchases.

Soft commercial construction over the past year and concerns over the import of foreign steel conduits have sent Atkore’s stock reeling from its previous highs around $190. I believe both these issues to be temporary setbacks. As interest rates decline, I expect that commercial construction projects, as well as projects in the residential and infrastructure sectors will revive demand growth for Atkore’s products. Foreign imports have put pricing pressures on Atkore’s products, as well as the rest of the industry, resulting in an overall decline in revenues while stagnating volumes. This obstacle is more complex, and politicians have been dragging their feet to address the issue despite damage to American manufactures. Luckily, there is growing legislative support in Washington to curb Mexico’s steel imports and what many are classifying as illegal dumping. I believe that in due time some form of legislation will pass providing protection for American manufacturers such as Atkore, especially in the case of a possible Trump administration who the company has acknowledged as being far more protective of American industry. Despite these issues and other market uncertainty I believe that secular trends will hold and Atkore will return to historical to slightly above historical growth trends.

At its current price in the mid-$80s, I believe Atkore is undervalued and offers modest upside potential with a solid margin of safety over the next few years. I expect that the company is engaged in heavy share repurchases at this time which will likely add to the upside as market conditions improve. Moving forward I intend to monitor economic data such as non-residential construction employment, the construction backlog indicator, the Architectural Billing Index, and Dodge Momentum Index, all of which serve as meaningful leading indicators for the industries Atkore serves.

Thanks for reading. I encourage your feedback and please share this to help Vidette Capital Research grow.