Kaspi.kz Deep Dive & Valuation ($KSPI)

Kaspi is a Kazakhstan-based fintech and e-commerce super app that integrates digital payments, banking, marketplace services, and financial technology into a single platform.

| AIX")

Kaspi.kz is a Kazakhstan based financial services and technology company that operates a two-sided super app for merchants/entrepreneurs and customers. Its super app integrates digital payments, e-commerce, financial services, and government services into a single, all-in-one platform. With its rapid growth, Kaspi has become a key driver of Kazakhstan’s digital transformation and is set to expand into other Central Asian markets, including Turkey, Uzbekistan, Azerbaijan, and Ukraine, positioning itself as a leading fintech and e-commerce provider in the region. Kaspi’s goal is to scale and expand its digital ecosystem to reach over 100 million customers, representing a sixfold increase from its current user base.

Kaspi traces its origins back to 1991, when it was established as Al Baraka Kazakhstan in Almaty, the largest city in Kazakhstan. In 1997, it was rebranded as Bank Caspian before being acquired in 2002 by entrepreneur Vyacheslav Kim, who envisioned integrating consumer lending and banking services with retail operations. To realize this vision, he partnered with Baring Vostok Capital Partners, where Mikheil Lomtadze was a partner. Recognizing Lomtadze’s expertise, he was appointed to the board of directors and, in 2007, became chairman. Under Lomtadze’s leadership, Kaspi underwent a profound transformation from a traditional bank into a leading fintech ecosystem, introducing innovative services such as online bill payments, e-commerce platforms, and, in 2017, the Kaspi.kz Super App, which integrates payments, marketplace services, and financial products into the Kazakh economy. In 2020, Kaspi entered the global financial markets with its listing on the London Stock Exchange (LSE). However, it voluntarily delisted in March 2024, citing low trading volume. In January 2024, Kaspi successfully completed an IPO on Nasdaq, under the ticker KSPI (Joint Stock Company Kaspi.kz), marking the first company from Kazakhstan to be listed on a U.S. stock exchange. The stock currently sees an average daily trading volume of approximately 260,000 shares on the Nasdaq.

Operations

Central to Kaspi’s operations is the Kaspi.kz Super App, the backbone of its digital ecosystem. The company operates two key apps: the Kaspi.kz Super App, designed for consumers, and Kaspi Pay, built for merchants and entrepreneurs. With approximately 14.7 million monthly active users (MAUs), the Kaspi.kz Super App serves as an all-in-one financial and lifestyle platform, offering digital payments, bank accounts, personal and auto loans, buy-now-pay-later (BNPL) financing, bill payments, e-commerce shopping, travel bookings, a loyalty rewards program, and more. On the business side, the Kaspi Pay Super App, used by approximately 737,000 active merchants, enables businesses to accept QR payments, process transactions, sell on the Kaspi Marketplace, advertise, access credit and tailored financial services, and more. Refer to the image below for a breakdown of each app’s respective offerings.

The integration between the Kaspi.kz Super App and Kaspi Pay enables a seamless interaction between consumers and businesses, creating a unified digital ecosystem. When a consumer makes a purchase—whether online through the Kaspi Marketplace or in-store using Kaspi QR payments, the transaction is processed entirely within Kaspi’s closed loop infrastructure. Payments move directly from the customer’s Kaspi account to the merchant’s Kaspi Pay account, eliminating the need for third-party processors. This direct connection allows for faster settlements, lower transaction costs, and greater control over the entire payment flow. Beyond payments, the integration extends to financing and commerce. Customers can access Kaspi Kredit to finance purchases instantly, while merchants using Kaspi Pay can qualify for business loans based on their sales history. Merchants who sell through the Kaspi Marketplace rely on the same infrastructure to manage transactions, offer installment plans, and advertise products to Kaspi.kz users. As a result, both apps continuously interact. Businesses benefit from increased sales and financial support, while consumers experience a streamlined purchasing and payment process. And all that data can be leveraged to tailor offerings and make more informed credit decisions.

Business Segments

Kaspi breaks its operations down into three major segments: Payments, Marketplace, and Fintech. There is actually a fourth segment of Government Services, but this is not meant to be revenue generative to the company. Let’s break these segments down further to give a better understanding of operations.

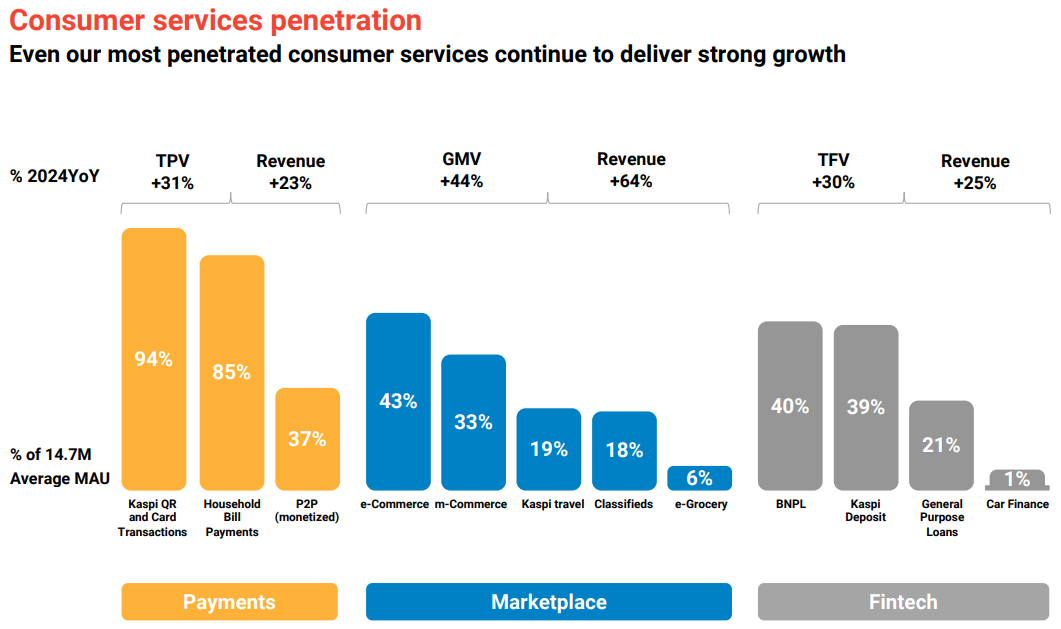

Payments are the bread and butter of Kaspi’s operations, facilitating transactions between and among merchants and consumers. It is its highest-margin business segment, generating ₸381,607 million in net income in 2024 with a 65% net margin. It is also the company's largest source of net income, contributing 36% of total earnings in 2024. Over the past five years, net income has grown at a CAGR of 68.8%, while segment revenue has expanded at a CAGR of 54.6%, highlighting both scalability and margin expansion. The payments platform has 13.6 million active customers and 737,000 active merchants, accounting for over 5.9 billion transactions in 2024. In 2023, Kaspi processed 78% of all payment network transactions in Kazakhstan, more than were processed by Mastercard and Visa combined. Total Payment Value (TPV), the total value of B2B and payment transactions made by active consumers within Kaspi’s payments platform, excluding free P2P and QR payments, was approximately ₸37,200 billion. TPV has grown at a CAGR of 60.9% over the past five years. The Payments take rate (the percentage of TPV that Kaspi captures as revenue) for the entire segment was 1.18%.

The Payments Segment consists of the following key services:

Consumer Services:

P2P Payments: Enables instant, commission-free money transfers between users via the Kaspi.kz Super App, with fees applied only to transfers to other banks’ cards (2.8% of transactions in 2023).

Kaspi QR: A widely accepted QR-based payment system allowing cardless transactions between consumers and merchants via the Kaspi.kz and Kaspi Pay Super Apps.

Kaspi Gold: A digital account and prepaid debit card used for online and in-store transactions, opened digitally with biometric verification via Kaspi ID.

Household Bill Payments: Allows users to pay recurring bills commission-free, covering utilities, mobile, internet, transportation, education, and taxes through the Kaspi.kz Super App.

Merchant Services:

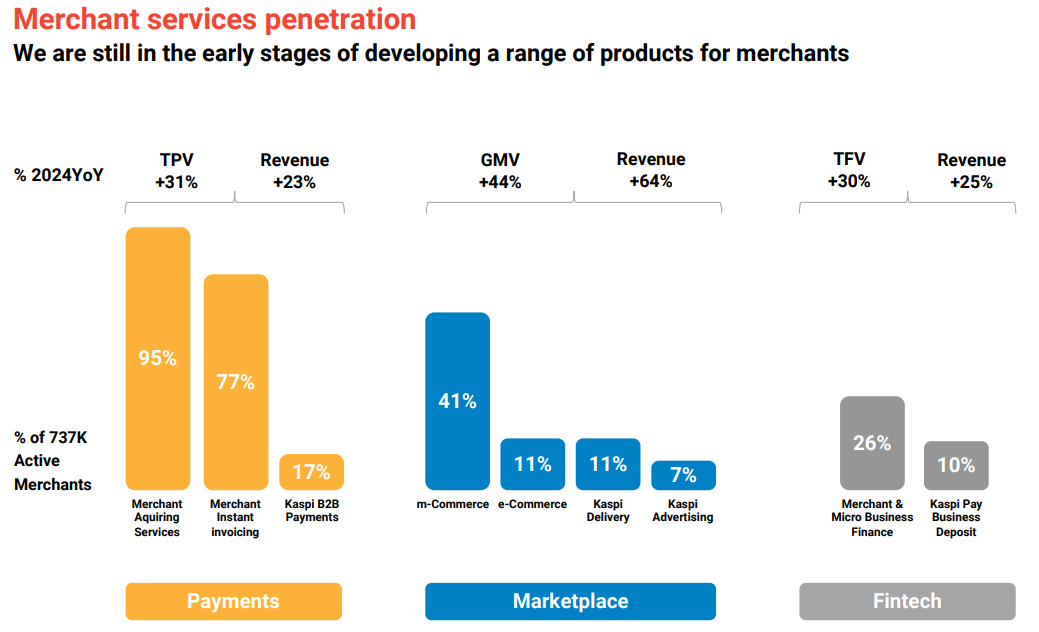

Merchant Acquiring Services: Allows businesses to accept in-store and online payments via Kaspi QR, Kaspi Gold, and third-party bank cards, supported by Kazakhstan’s largest POS network with 538,000 m-POS and Smart POS devices as of fiscal 2023. As of 2024, there were 257 thousand active merchants using a POS register transacting over ₸1.2 trillion.

Merchant Instant Invoicing: Enables seamless integration of invoicing and bill processing with the Kaspi.kz Super App for instant settlements.

Kaspi B2B Payments: Provides digital invoicing and instant settlement solutions for businesses, forming the foundation for future B2B financial services. This is the fastest growing service under Kaspi’s Payments Segment

Kaspi Shopping Register: A digital cash register integrated with Kaspi Pay’s POS network to help merchants accept payments while complying with tax regulations.

Kaspi Pay Business Account: A digital merchant account created upon onboarding onto the Kaspi Pay Super App.

Tax Reports & Payments: Assists merchants in calculating taxes and filing tax reports through the platform.

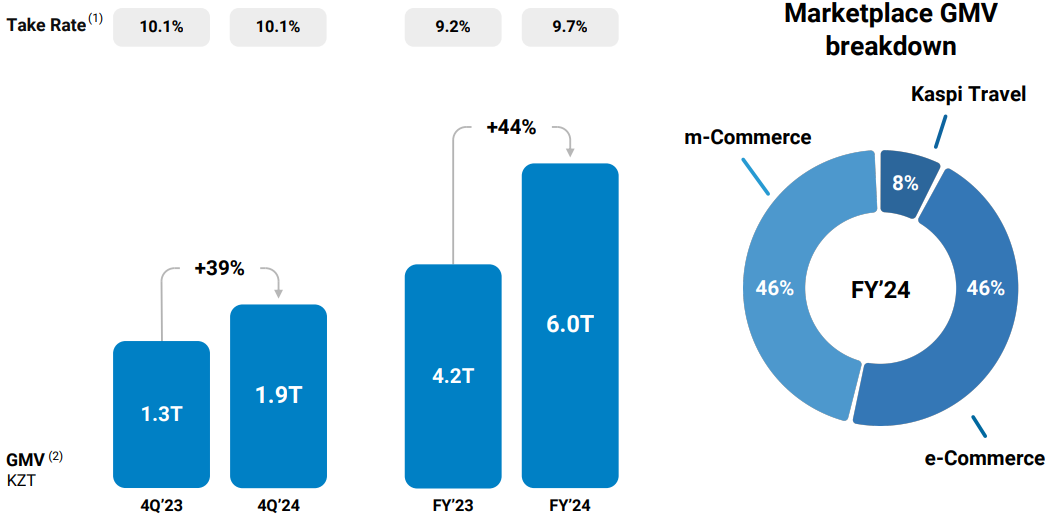

Marketplace is Kaspi’s e-commerce and services platform, allowing users to shop for a wide range of products, book travel, and pay for various local services. It connects consumers with merchants and enables direct, digital transactions through the Kaspi.kz Super App. Similar to Amazon, it primarily operates as a third-party (3P) model, except in e-Grocery and E-Cars, allowing merchants to sell directly to consumers. It is Kaspi’s second-largest business segment by both revenue and net income, accounting for 33% of total net income in 2024. The segment’s net margin was 47.5% in 2024, down from 55.3% in 2023, reflecting Kaspi’s expansion into lower-margin business units such as e-Grocery and e-Cars. Gross Merchandise Value (GMV)—the total transaction value of goods and services sold within Marketplace—reached ₸6,000 billion in 2024, supported by 233.6 million purchases, with GMV growing at a 5-year CAGR of 57.1%. The Marketplace take rate was 9.7% continuing a steady climb over the past 5 years.

The Marketplace Segment consists of the following services:

3P Marketplace (Third-Party Model):

E-Commerce: Allows consumers to browse, purchase, and receive delivery of products through the Kaspi.kz Super App, with support from merchant reviews, ratings, videos, and flexible payment and delivery options supported by Kaspi’s Fintech and Payments platform. E-commerce also consists of segments, E-Grocery and E-Cars which I break down further below. In 2024 E-Commerce GMV was ₸2800 Billion supported by 101 million purchases. The E-commerce take rate was 11.3% continuing a steady climb upward. E-Commerce is the fastest growing service within Kaspi’s Marketplace Segment, a trend that is likely to continue with the recent acquisition of Turkish e-commerce company, Hepsiburada.

M-Commerce: Brings a digital shopping experience to physical stores, allowing merchants to list business profiles, store locations, and operating hours. Through the Kaspi.kz Super App, consumers can research products and services and complete purchases in-store via Kaspi QR and BNPL (Buy Now, Pay Later) products. M-Commerce has grown at a three-year CAGR of 37.5%, reaching a GMV of approximately ₸2,700 billion in 2024, driven by 115.1 million purchases. The M-Commerce take rate for 2024 was 9.1%, continuing a steady climb from 2021.

Kaspi Travel: Provides consumers with the ability to purchase rail and air tickets as well as international vacations packages, fully integrated with Kaspi Gold and BNPL for seamless payments. Kaspi Travel was launched in 2020 following the acquisition of Santufei, one of Kazakhstan’s leading airline ticket platforms. They have since expanded to include rail tickets and launched Kaspi Tours, a vacation package marketplace. Kaspi travel is the largest travel agency in Kazakhstan. In 2024, Kaspi Travel brought in a GMV of 471 billion up 34% over 2023, supported by 17.6 million ticket purchases and a take rate of 4.6%. Kaspi travel was 8% of the Marketplace Segment GMV.

Kaspi Classifieds: A marketplace allowing businesses and consumers to advertise for new and used goods, services, and job listings. Kaspi is the majority shareholder in Kolsea Group (50.76%) which operates Kolesa.kz, Krisha.kz, and Market.kz, leading classified sites in areas of automotive, real estate, and general classifieds. Kolsea Group also owns Autoelon.uz a car marketplace in Uzbekistan and Digital Classifieds LLC mobile classified app in Azerbaijan.

1P Marketplace (First-Party Model):

E-Grocery: provides free home delivery of groceries within 24 hours, targeting weekly household shopping with a focus on high average ticket size and strong unit economics, all through the Kaspi.kz Super App. Unlike other marketplace services, Kaspi operates e-Grocery as a 1P model, managing rented dark stores, logistics, and inventory to ensure quality and efficiency. Kaspi first entered e-Grocery in 2021 through a partnership with Kazakhstan’s largest food retailer, Magnum, before acquiring a 90.01% stake in Magnum E-commerce Kazakhstan in 2023. While e-Grocery has grown significantly in recent years, it still accounts for only 5% of e-Commerce GMV, with plans to expand into two new cities in the coming years. In 2024, e-Grocery GMV reached ₸135.1 billion, supported by 9.6 million purchases across 858,000 active customers.

Car E-Commerce: Streamlines the buying and selling of used cars, integrating vehicle search, selection, and legal registration within Kolesa.kz. The platform also offers online car financing, fully integrated with Kaspi’s Fintech Platform. Car E-Commerce brought in ₸239 billion in 2024 accounting for 28% of total ecommerce GMV.

Delivery Services:

Kaspi Delivery Smart Logistics Platform: Integrates third-party delivery partners with e-Commerce orders, offering multiple fulfillment options, including door-to-door delivery, express delivery, in-store pickup, and Kaspi Postomats. In 2024, Kaspi Delivery handled 99 million orders, 84% of which were free delivery, with 47% arriving in less than 48 hours.

Kaspi Postomats: Postomats are automated parcel machines (APMs) that allow customers to pick up their online orders securely and conveniently by entering a code or scanning a QR code. As of 2024, Kaspi operates 8,030 Postomats, making it a key part of its delivery network, improving efficiency and reducing last-mile delivery costs. Postomats accounted for more than 50% of e-Commerce deliveries in 2024. It is estimated that 80% of active customers are located within a five minute walk of the nearest Postomat.

Advertising Services:

Kaspi Advertising: Enables merchants to run targeted ad campaigns within the Kaspi.kz Super App, including sponsored product listings, suggested products, and banner ads. Merchants can manage and track ad performance through the Kaspi Pay Super App. As of their fiscal 2024 earning presentation, 51 thousand merchants and brands were utilizing Kaspi Advertising. Like delivery, advertising is a value added service that allows Kaspi to earn a higher take rate on Marketplace transactions.

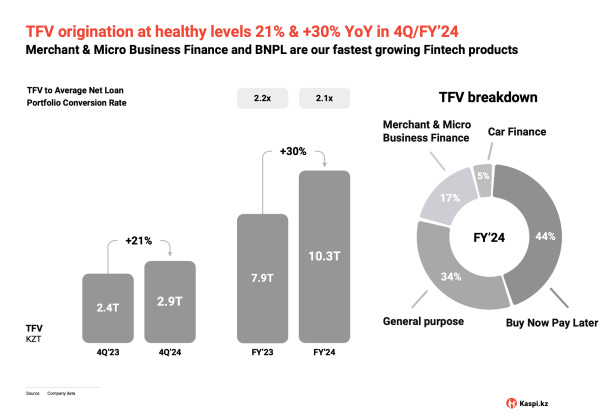

Fintech is Kaspi’s banking and financial services platform providing integrated financial services that support both consumers and businesses, offering a range of lending and credit solutions directly through the Kaspi.kz Super App. By utilizing transaction data from its Payments and Marketplace segments, Kaspi enhances credit accessibility and decision making, enabling financing options that drive both consumer spending and merchant growth. Fintech is Kaspi’s largest segment by revenue, generating ₸1,281 billion in 2024, but it is the smallest contributor to net income, accounting for 31% of the total. Over the past five years, net income from the Fintech segment has grown at a CAGR of 18.3%, with a net income margin of 25% at the end of 2024. Total Finance Value (TFV)—the total value of loans issued and originated within the year—amounted to ₸10.3 trillion, while the average net loan portfolio stood at ₸4,900 billion. The segment’s Fintech Yield, defined as the sum of interest income on loans and fee revenue divided by the average net loan portfolio, was 24%. Kaspi also had 5.7 million active deposit customers and 6.4 million active loan customers in 2024.

The following services are supported by the Fintech Segment:

Consumer Services:

Buy-Now-Pay-Later (BNPL): Enables consumers to finance purchases on the Marketplace Platform, with short-term interest-free financing for up to three months and longer-term options during promotions like Kaspi Juma (Kaspi equivalent of Amazon Day x 3). BNPL is the Fintech Segments largest contributor to TPV at 44% for 2024.

General Purpose Loans: Unsecured loans for everyday purchases outside the Marketplace Platform.

Car Finance: Online car loans for vehicle purchases through Kolesa.kz, with the purchased car acting as collateral.

Kaspi Deposit: A digital savings account available through the Kaspi.kz Super App, denominated primarily in Kazakhstani tenge and U.S. dollars, offering both current and term deposit options.

Merchant Services:

Merchant & Micro Business Finance: Provides working capital loans to merchants and small businesses, with loan eligibility linked to their turnover and GMV on Kaspi’s Payments and Marketplace Platforms. This incentivizes businesses to process more transactions through Kaspi, strengthening network effects.

Buy-Inventory-Now-Pay-Later: Offering merchant financing where Kaspi pays the supplier immediately and the merchant pays it back within 30 days. Recently rolled out in Q3 of 2024.

Business Deposit: Dedicated deposit accounts for merchants that were also recently rolled out. In their Q4 2024, management stated that around 10% of merchants were already using business deposit. Business Deposit & BINPL are two additional reasons for merchants to transact and keep more of their funds with Kaspi and will likely boost B2B payments as well.

Government Services is Kaspi’s GovTech platform integrated into the Kaspi.kz Super App, providing digital access to essential government services. Users can store and access digital ID documents, renew driving licenses, transfer car ownership, register marriages, and obtain birth certificates, while entrepreneurs can register businesses, calculate and pay taxes, and file tax reports. Though not revenue-generating, the segment enhances user engagement and strengthens synergies across Kaspi’s ecosystem. By integrating government services into the Kaspi.kz Super App, it increases platform usage, making customers more likely to use car loans, vehicle registration, Kaspi Travel, and other services due to the convenience of having everything in one place. In 2024, Kaspi reported that over 11.8 million people had visited their Government Services platform via the Kaspi.kz Super App.

Business Infrastructure

Kaspi's physical and technological infrastructure supports its digital operations through a combination of data centers, financial service points, proprietary software, and logistics networks. The company operates four dedicated data centers, including one for testing, which are managed under Kaspi Cloud, a subsidiary responsible for data storage, maintenance, and processing. This infrastructure facilitates transaction processing, risk assessment using machine learning models, and the operation of Kaspi’s digital services. The company centralizes all credit decisions, verification, and underwriting processes at its headquarters in Almaty to ensure uniformity and oversight in its lending operations.

In addition to its cloud infrastructure, Kaspi maintains a nationwide physical presence, operating over 3800 payment kiosks, 3300 ATMs, and 150 Kaspi Kartomats, which provide users with access to deposits, wallet top-ups, and cash withdrawals. The company also has more than 115 Kaspi.kz Outlets that serve as in-person customer service centers, offering assistance with financial products and access to Kaspi Postomats. Kaspi operates a 24/7 call center, Kaspi Allo, and an AI-powered virtual assistant, Ruslan, which handled over 14 million customer interactions in 2023. To support its Marketplace and logistics operations, Kaspi developed the Kaspi Delivery Smart Logistics Platform, which integrates with third-party couriers, uses smart routing and real-time tracking, and manages the last-mile delivery Postomats Network. As of December 2023, Kaspi Reported that approximately 2,500 couriers, 60 delivery companies and 2,000 sorting warehouse employees were connected to their delivery platform.

Revenue Generation

Kaspi generates revenue through interest income, fees, and commissions earned from transactions, lending, and value-added services across its ecosystem. Its revenue streams are primarily derived from three core segments, each of which is monetized through a combination of interest margins, transaction fees, and take rates on merchant sales. The Fintech segment earns revenue primarily through interest income on deposits, personal loans, auto loans, and BNPL financing, as well as loan origination and service fees. It also generates from business lending, where merchants using Kaspi Pay can access financing, contributing to additional interest income and service charges.

In the Payments segment, revenue is generated through take rates on transactions, as Kaspi charges businesses a percentage of every payment processed via Kaspi QR, Kaspi Gold debit cards, and Kaspi Pay terminals. Additional revenue streams include fees from peer-to-peer (P2P) transfers, bill payments, B2B payments, and other financial transactions, as well banking service fees for premium financial products. Meanwhile, the Marketplace segment generates revenue through take rates on merchant sales, where businesses pay a commission on transactions made through the Kaspi Marketplace. Kaspi also earns revenue from advertising fees, as merchants pay for promotional placements within the Kaspi.kz Super App, and from logistics and delivery fees.

Kaspi’s take rates on e-commerce and payments are highly competitive compared to industry peers. While the company does not directly compete with other super apps, an analysis of major global players such as MercadoLibre, NU, Allegro, Alipay, WeChat (Tencent), Yandex, and Paytm suggests that Kaspi maintains some of the most competitive take rates and fee structures in the market. They, by far, enjoy some of the nicest net margins in the industry at over 40%, although I expect these will contract in the coming years as Kaspi grows and onboards less profitable verticals and expands internationally.

Macroeconomics and Kazakhstan as a Country

Kazakhstan is the world's largest landlocked country and boasts a resource-rich economy heavily reliant on oil, gas, and minerals such as copper, zinc, and uranium. Key economic drivers include oil and gas production, mining, agriculture, and a growing services sector, particularly in finance and IT. The country's vast uranium reserves have attracted interest from major world powers seeking investment opportunities and stronger geopolitical ties in the region. In 2024, Kazakhstan’s GDP reached approximately $288 billion USD, with a five-year compound annual growth rate (CAGR) of 9.6%. One example of investment in the region contributing to growth has been China’s Belt & Road Initiative (BRI), which has positioned Kazakhstan as a critical transit hub, boosting regional connectivity and driving infrastructure development. The country's population reached 20.6 million in 2024, with a five-year CAGR of 2.2%, supporting economic expansion and labor market growth.

Kazakhstan is a unitary presidential republic with a strong executive branch, where the President holds significant authority over the government. The current president, Kassym-Jomart Tokayev, is serving a seven-year term until 2029 after running on a platform of political, economic, and social reforms aimed at modernizing the country. Since taking office, Tokayev has worked to create a more balanced governance model by decentralizing power, limiting presidential terms, curbing oligarch and family influence, strengthening anti-corruption agencies, introducing whistleblower protections, and investigating officials linked to the former administration. Historically, Kazakhstan has not been a top destination for foreign investors, but Tokayev is actively working to improve the investment climate and position the country as an emerging hub for technology, finance, and logistics. Tokayev has frequently acknowledged Kaspi.kz and its CEO, Mikhail Lomtadze, for their contributions to Kazakhstan’s digital economy and their role in modernizing the financial and technology sectors as the country seeks to diversify beyond its traditional reliance on natural resources. I believe Kaspi’s close relationship with the government is a strategic advantage for the company. Its government services segment ensures direct engagement with top officials, strengthening its position in the regulatory and economic landscape. Additionally, the widespread adoption of the Kaspi.kz SuperApp and its ability to leverage vast amounts of consumer data likely provide valuable insights for economists and policymakers, further solidifying Kaspi’s role in Kazakhstan’s digital and financial infrastructure or at least earning them a seat at the table.

Refocusing on Kaspi itself, the company’s performance is influenced by the broader economic environment and macroeconomic conditions in Kazakhstan and the surrounding region. Its business segments are directly impacted by factors influencing disposable consumer income, including employment levels, inflation, business conditions, consumer credit availability, interest rates, tax policies, and fuel and energy costs. Inflation, in particular, has been a significant headwind for both Kaspi and the Kazakh economy in recent years. As a resource-dependent nation, Kazakhstan's government revenues and the tenge's exchange rate are highly sensitive to fluctuations in oil and other commodity prices. Additionally, COVID-19, global supply chain disruptions, and geopolitical tensions—particularly the Russia-Ukraine war—have further strained economic conditions. The spillover effects of sanctions, rising energy costs, capital flight, and currency depreciation have driven up the cost of imports, exacerbating inflation and creating a challenging consumer environment. Market inefficiencies, including state-owned enterprises and monopolies, limiting competition have compounded these issues, making it increasingly difficult for businesses and consumers alike to navigate the economic landscape. Kazakhstan’s National Bank (NBK) currently maintains one of the highest interest rates in the region, standing at approximately 15% as of early March 2025. Kaspi has identified inflation as a key driver of rising expenses, which has also put pressure on the profitability of its Fintech segment. If the Russia-Ukraine war reaches a resolution or a ceasefire in the near future, the region will likely benefit from reduced inflation interest rates over the coming years.

Taxes and Regulations

Kaspi operates under strict regulatory oversight in Kazakhstan, primarily from the National Bank of Kazakhstan (NBK) and the Agency for Regulation and Development of the Financial Market (ARDFM). As a systemically important financial institution, it must meet stringent capital adequacy and liquidity ratios, with potential restrictions on dividends if thresholds are not maintained. It is also classified as a Significant Payment Services Provider, requiring licensing, anti-fraud measures, and transaction monitoring. Regulatory risks extend to Anti-Money Laundering (AML) and Counter-Terrorism Financing (CTF) compliance, mandating strict KYC, transaction monitoring, and reporting of suspicious activity within 24 hours. Foreign ownership is restricted, requiring regulatory approval for stakes above 10%, with heightened scrutiny beyond 25%. Interest rate caps (56%) on consumer loans impact lending profitability, while Kazakhstan’s Personal Data Law mandates local data storage and explicit user consent, which can result in higher compliance costs. Kaspi does trade as an ADR in the United States, so shareholder rights are limited.

Kazakhstan’s has an evolving legal landscape, including uncertain regulatory interpretations and government intervention (e.g., the 2023 Law on the Return of Illegally Acquired Assets). This can present both risks and uncertainties although I believe that Kaspi’s dominant market position and compliance framework provide a level of stability. None the less, it’s something for investors to monitor. With regard to taxes, I’ll note that Kazakhstan’s economic ministry is working to raise corporate taxes on banks from 20% to 25% to counter government budget deficits.

Competitive Advantages

Kaspi has built a robust competitive moat through its integrated digital ecosystem, extensive market presence, and Super App model. By seamlessly integrating financial services, payments, e-commerce, and government solutions, Kaspi benefits from strong network effects, high customer retention, and significant data advantages. These factors reinforce its leading position in Kazakhstan's digital economy and provide a scalable foundation for expansion into other markets. The following are what I believe to be notable competitive advantages for Kaspi.

Network Effect: The Kaspi.kz Super App benefits from strong self-reinforcing network effects and engagement. The platform integrates multiple services—payments, shopping, finance, and government services, creating a highly engaging digital environment for both consumers and merchants. The more users engage with Kaspi’s ecosystem, the more attractive it becomes for merchants, which in turn attracts more consumers. The convenience and one-stop nature of the app allows Kaspi to easily cross sell customers and merchants into other services. As of its 2024 full-year presentation, Kaspi reported 14.7 million monthly active users (MAU) and 10.1 million daily active users (DAU), resulting in a DAU/MAU ratio of 68.7%. This places Kaspi among the super apps with the highest user engagement rates.

Brand Strength: Kaspi is one of Kazakhstan’s most recognized and trusted brands in fintech and digital commerce. The company has maintained exceptionally low churn rates among both customers and merchants while steadily expanding its market reach. Kaspi’s Payment segment boasts over 90% penetration, underscoring its deep integration into daily life. Meanwhile, other segments continue to gain traction. Kaspi has a Net Promoter Score rating of 78, indicating strong customer satisfaction and loyalty, well above the 70+ threshold considered “world-class.” The company places significant emphasis on this metric, using it as a key driver for innovation and strategic decision-making. Kaspi’s strong brand reputation also enables it to attract and retain top talent in the region, further strengthening its competitive position.

Low Cost Operations: Kaspi's scale and operational efficiency position it as a highly competitive, low-cost operator, as reflected in its exceptional net margins. The company has prioritized developing its own technology and systems in-house, allowing for greater cost control and minimizing reliance on third-party providers. Additionally, strong brand reputation reduces costs in sales, marketing, and customer acquisition, making it more challenging for competitors to enter highly penetrated business lines. The super app model inherently benefits from economies of scale, as more customers join the platform, fixed costs are spread over a larger user base, increasing margins. Although Kaspi is not competing directly with other super apps at this time, I believe this gives Kaspi a cost advantage over competitors confined to specific segments, as they lack the cross-platform synergies that drive cost efficiencies. Another key area of cost efficiency is Kaspi’s last-mile delivery network, Postomats.

Data Advantage: In the nature of Kaspi’s business the company collects a vast amount of data on customer behaviors that they can leverage to drive further engagement, cross sell products and services, improve logistics, advertise, and continue to build out their ecosystem. I believe Kaspi benefits most from this in their Fintech Segment where they are able to leverage customer information and behaviors to determine credit and transaction risk. In their 2023, 20F Kaspis states, “Our risk models analyze over 4,380 data points in order to assess the credit risk of a consumer and allow us to make 99.9% of consumer loan approvals within six seconds. This results in consistently low Cost of Risk in our Fintech Platform…” Credit risk was 2%, and 2.1% for 2023 and 2024 respectively. I believe Kaspi has one of the most comprehensive credit profiles of any company in Kazakhstan, and the company has a history of improving its percentage of Non-Performing Loans (NPLs), which was 5.4% at the end of 2024.

First Mover Advantage and Barriers to Entry: Kaspi was one of the first fintech players in Kazakhstan to integrate banking, payments, and e-commerce into a single super app. Its early dominance allowed it to build a strong user base, establish a solid regulatory position in Kazakhstan’s fintech and e-commerce sectors, as well as the government itself, and scale to a level where competitors are highly deterred by the costs to simply catch up. Kaspi’s high brand recognition and integrated ecosystem have created a high level of customer stickiness making direct competition unlikely.

Scalability: The Kaspi.kz Super App is highly scalable, allowing the company to grow organically and serve a larger user base with relatively low capital expenditures. By leveraging its integrated platform, Kaspi has demonstrated a proven ability to cross-sell services and increase penetration within its existing customer base, driving revenue growth without significant acquisition costs. I believe Kaspi’s scalability will be critical to their international expansion, but this remains relatively untested with over 95% of revenue coming from Kazakhstan.

Growth Outlook

Central to Kaspi’s investment thesis is its strong growth outlook. Since 2019, the company has expanded its MAUs from 5.7 million to 14.7 million in 2024, now representing 71% of Kazakhstan’s estimated 20.6 million population. Over the same period, revenues grew from ₸602.8 billion to ₸2.5 trillion, achieving a five-year CAGR of 37.6%, while earnings per share (EPS) grew at a CAGR of 39.5%. Kaspi aims to expand their user base to serve 100 million customers. A significant step toward this goal was the 2024 acquisition of a 65.4% stake in Hepsiburada, a leading e-commerce platform in Turkey (population 87 million). Although early, this acquisition puts Kaspi’s addressable market in range of achieving their goal.

There are three major drives to Kaspi’s growth: International expansion and acquisitions, continued penetration and adoption of new and existing services, and return of stability in the region. My goal here is not to project growth rates across various business units. I cannot predict the extent of penetration for new services or the timing and success of international expansion, particularly in uncertain markets like Ukraine. Instead, my goal is to analyze Kaspi’s recent performance and future opportunities and, using a reverse discounted cash flow (DCF) model, determine the minimum and probable rate of growth required to justify the stock’s current valuation.

International Expansion and Acquisitions: Beyond Turkey, Kaspi is also targeting Azerbaijan (population 10.5 million), Uzbekistan (36.4 million), and Ukraine (37 million) as key markets for future growth. In 2023, Kaspi reported active international operations in the countries of Azerbaijan, Uzbekistan, and Ukraine, however these have primarily been limited to the Kolesa classified businesses of which Kaspi took a controlling stake in in 2023. Kaspi’s international expansion plan strategy is to follow a structured approach that leverages its payments business as an entry point into new markets, gradually expanding into M-Commerce and eventually E-Commerce.

Acquisitions appear to be a key factor in Kaspi’s international expansion plans. In 2021, the company acquired Portmone, a Ukrainian payment platform. The acquisition represents less than .1% of assets and little progress has been made due to the ongoing conflict in the region. Kaspi plans to reprioritize this acquisition when stability returns to the region.

In 2024, Kaspi acquired a 65.4% stake in the Hepsiburada, substantially expanding their addressable market into Turkey whose GDP and retail market is 4x the size of Kazakhstan’s. Hepsiburada is estimated to have a 16% penetration in Turkey. The acquisition was structured with an initial cash payment of $600 million, with an additional $526.9 million due within six months of closing, which Kaspi plans to fund through operating cash flow in the first half of 2025. Hepsiburada was hit hard by the Covid 19 pandemic, but management has successfully returned the company to profitability. By late 2024, the platform had 12 million active customers, 100,000 active merchants, and generated $3.5 billion in GMV. Kaspi intends to maintain Hepsiburada as a distinct brand while integrating its payments and e-commerce technology into the platform. Kaspi will not include Hepsiburada's financial results in its 2025 guidance. Acquisitions are expected to remain a core part of Kaspi’s growth strategy, supporting both international and domestic expansion, as well as entry into new business lines.

Continued Penetration and Adoption of New and Existing Services: Kaspi continues to see further adoption and higher usage of its services. Payment’s volume has consistently seen a 30% to 40% annual growth rate, average monthly transactions per customer are on the rise reaching 73 in 2024, and MAU/DAU is also on a steady incline. Just about every business line has seen double-digit growth despite headwinds of increased inflation and regional instability. Within the Fintech segment, Merchant & Micro Business Finance and BNPL are the fastest growing products. In the Fintech segment, Merchant & Micro Business Finance and BNPL remain the fastest-growing products. Within Marketplace, E-Grocery and E-Cars lead in expansion. New offerings such as Merchant Deposits, BINPL, and Gift Cards have been well received, driving increased customer engagement across the platform.

Many of Kaspi’s business lines are still in the early stages, with relatively low but steadily increasing penetration. Significant growth opportunities remain across the board, particularly in E-Commerce, E-Grocery, deposits, and value-added services such as delivery and advertising. While penetration levels may not reach the 85%+ seen in Kaspi’s Payments segment, I anticipate a gradual convergence over time, driving sustained expansion. Given these dynamics, I have no difficulty expecting continued low to mid double-digit growth for the company over the next five years. Additionally, as the use of value-added services grow, take rates will continue to climb particularly in Marketplace, however I expect Kaspi will keep them very competitive. Delivery in particular has yet to scale meaningfully, so as delivery volumes increase we will likely see reduced unit costs in the business line.

Return to Stability in the Region: Kazakhstan's geopolitical climate has improved in recent years, making the country more attractive to investors. Efforts to combat corruption, along with increasing inflows of foreign capital, are bolstering confidence in the market. As Kaspi gains momentum on U.S. exchanges, it will likely benefit from higher valuation multiples.

The COVID-19 pandemic and the Russia-Ukraine war have taken a toll on the region, driving high inflation and escalating concerns about geopolitical instability, both of which have weighed on economic growth. Kaspi’s Fintech segment has been particularly affected, as elevated funding costs from high interest rates have constrained profitability. While peace talks between Russia and Ukraine have yielded little progress, there is growing optimism that the conflict may be nearing its resolution. This would serve as a catalyst for Kaspi who is likely to benefit from declining inflation, lower interest rates, and increased consumer confidence. Although premature, I believe that Kaspi is well positioned to benefit from investment inflow particularly in Ukraine, as the country embarks on post-war reconstruction.

In Kaspi’s 2024 earnings report they guided for the following: “We expect Kaspi.kz to deliver another strong year of profitable growth and expect consolidated net income growth around 20% YoY for 2025. This guidance excludes any impact from our business in Türkiye.”

Competition

The Kaspi.kz Super App does not have direct competition, as most of the competition it faces comes at the level of its individual business units. These competitors are generally smaller companies with significantly less access to capital than Kaspi. The company does compete with global players particularly in the payments sector, but Kaspi remains the dominant force in the Kazakhstan market. I do not find a deep analysis of Kaspi’s competitors of great value, but here is a list of key players across its major segments.

E-Commerce – OLX.kz, Ozon.kz, Wildberries.kz

Payments – Sulpak.kz, Paypal, Apple Pay

Fintech – Halyk Savings Bank, National Trust Bank

I believe there is a small risk of Chinese super apps attempting to expand into Kazakhstan or the broader Central Asian market in the future. However, they would likely face significant regulatory hurdles, and even if they managed to enter, I am skeptical that they would be able to attract a substantial number of customers away from Kaspi.

Management

Vyacheslav Kim and Mikheil Lomtadze both hold a substantial stake in the company they founded. Only around 27.7% of the shares outstanding are held by public investors whereas the rest is owned by the two cofounder, three investment firms and other members of management. Vyacheslav Kim alone holds a quarter of Kaspi’s outstanding shares. Vyacheslav is the Chairman of the Board of Directors. He appears to spend a great deal of his time on government and international relations as well as ensuring that the company is compliant with government regulations particularly with the US, EU, and other sanctioned regimes such as Russia.

Mikheil Lomtadze is the CEO of Kaspi and member of the Board of Directors. He is a purpose driven individual, focused on building a user centric ecosystem with products and services that provide actual value to customers. He has a background in consulting and private equity, along with strong operational expertise. Lomtadze takes a cautious and strategic approach to acquisitions, focusing on sustainable expansion. Under his leadership, many of the business lines added to the Kaspi.kz Super App have achieved profitability immediately or within a year. His approach suggests a focus on customer needs as a core driver of the company’s strategy, with an emphasis on long-term value creation that benefits both customers and shareholders. In a question regarding the company maximizing take rates, Lomtadze replies, “But don’t expect us that we’ll be charging 20% to 30% like other marketplaces do because we believe that is counterproductive and that means not creating the value for merchants but actually taking value from them.”

Other key members of Kaspi’s management team include COO Pavel Mironov, CFO Tengiz Mosidze, and Yuri Didenko, who leads the Capital Markets division. For more information click the link to Kaspi’s governance page.

Lomtadze’s philosophy is embedded in Kaspi’s operations, with customer feedback playing a central role at every stage, from product development to performance evaluation. Consumer insights are integrated into the company’s key performance indicators (KPIs), directly influencing how employees are assessed. To gather feedback, Kaspi leverages their call centers and push notifications, prompting users to evaluate service quality and provide input shortly after use. This continuous feedback loop helps refine offerings and align business decisions with customer needs.

Overall, Kaspi appears to have a strong management team, and I appreciate their customer-centric approach as well as their measured strategy in expanding into new business lines and international markets. With the higher rates of corruption in the region that Kaspi operates, I do plan to more closely monitor the activities of management.

Capital Allocation

Kaspi’s primary capital allocation focus is growth, though the company has taken a cautious approach in recent years due to regional uncertainty. It maintains a low debt profile and has periodically repurchased shares, including the buyback of four million shares in fiscal 2024. The company has a history of paying dividends but has consistently stated that they may be redirect capital if significant growth opportunities arise. With the acquisition of Hepsiburada and expansion into Turkey, management has chosen to discontinue the dividend for the time being to prioritize growth. The company plans to update shareholders on the potential to return excess cash during the second half of 2025.

Risks

The following is a list of what I believe to be the most relevant risks to an investment in Kaspi:

Macroeconomic Risks: Kaspi and its customer base are sensitive to the economy of Kazakhstan. An economic downturn resulting in decreased consumer confidence, availability of credit, increase in unemployment, and inflation would have a negative effect on the usage of Kaspi’s services. If the Kazakhstani economy weakens, consumer spending on Kaspi’s Marketplace and Payments platforms could decline, negatively affecting revenue.

Inflation and Exchange Rate Volatility: Investing in Kaspi’s US ADR carries currency and inflation risks due to the company's reliance on the Kazakhstani Tenge while trading in USD. High inflation in Kazakhstan has led to tenge depreciation, reducing Kaspi’s USD-equivalent earnings, dividends, and valuation for ADR holders. For reference, the Tenge has lost about 20% of its value compared to the dollar over the past five years, most of which was the result of geopolitical instability in the region. Historically, the Tenge has experienced higher levels of inflation than the US dollar and this is a trend I expect to continue. Further currency devaluation could erode investor returns, even if Kaspi’s business performance remains strong. While I expect Kazakhstan’s inflation to stabilize as regional conditions improve, I must weigh the long-term investment appeal of Kaspi against the potential for renewed inflationary pressures, particularly if geopolitical instability resurfaces. Which brings me to the next risk.

Geopolitical Risks: Conflicts like the Russia-Ukraine war and Middle East instability can indirectly impact Kazakhstan’s economy and investor sentiment. Historically, regional conflicts have led to higher energy and commodity prices, driving inflation in Kazakhstan and prompting the National Bank of Kazakhstan to raise interest rates to stabilize the economy. Regional conflicts have also disrupted supply chains, a challenge further exacerbated by trade restrictions and economic sanctions imposed on key neighboring countries. The financial sector remains particularly vulnerable, facing higher interest rates, tightening liquidity, and an increased risk of loan defaults, all of which could pressure profitability and economic stability. Weighing heavily on the region right now is the Russia-Ukraine conflict. A resolution to the conflict appears to be underway (changing by the hour) and could serve as a positive catalyst for the region’s economic recovery. However, investors should remain mindful of potential for prolonged instability or the emergence of new conflicts, which could further disrupt economic conditions.

Regulatory and Legal Risks: Kaspi is subject to an array of regulatory compliance and evolving financial regulations both domestically and internationally. The Kazakhstani government may impose new regulations that could limit Kaspi’s growth or limit the extent of its business. Kazakhstan’s legal system is changing, creating uncertainty around compliance and business operations. Kaspi also faces anti-money laundering and sanctions laws, with non-compliance leading to fines or account freezes. As a major payment services provider, it is subject to strict oversight. Foreign ownership rules can add an additional layer of risk and uncertainty.

Expansion Risks: With Kaspi’s setting its sights on international expansion, there are risks that the company fails to successfully integrate acquisitions or navigate foreign regulatory hurdles. Each market has unique legal, financial, and competitive landscapes, requiring Kaspi to adapt its business model, technology, and compliance processes. Managing foreign operations also increases currency risk, capital allocation complexity, and potential geopolitical exposure, which could strain profitability. Super Apps are dependent upon their brand image and were the Kaspi brand to be damaged it may weigh down on its ability to expand into new markets.

Valuation

I am taking a multi-method approach to valuing Kaspi. Using a discounted cash flow model and a reverse discounted cashflow model, I estimate a base case fair value of Kaspi at around $115 per. This assumes a ROIC of 20%, and current free cash flow growth of 18% in the near term, gradually declining over time. Given Kaspi’s exposure to emerging markets and currency risks, I am applying a 16% discount rate. I have modeled for lower margins as a significant portion of the company’s growth is likely to come from lower margin business units in the medium term. If the Kazakhstani tenge stabilizes and inflation returns to 2019 levels, I believe a valuation of $130+ per share would be reasonable.

With respect to valuation ratios, Kaspi currently trades to the low end of its historical price to earnings, EV/EBITDA, and price to sales. For fiscal 2024, the company reported earnings of $10.35 per share, resulting in a P/E ratio of approximately 9, with a forward P/E of 7.7. Its EV/EBITDA is currently at 4.45, with a forward EV/EBITDA of 4.15, which is historically low.

Where Kaspi really starts to look undervalued is on a peer comparison basis. Other publicly traded super app companies include Tencent ($TCEHY), Alibaba ($BABA), Allegro ($ALEGF), NU Holdings ($NU), and MercadoLibre ($MELI). Kaspi is a fraction of the size of these other super apps with Allegro being the closest, however it is growing at a high rate. Based on the peer multiples, we could see a potential doubling in the stock price. MercadoLibre and NU Holding have a presence in South America and much like Kaspi have experienced high levels of inflation and currency risk, particularly in Argentina.

Kaspi appears particularly undervalued when compared to its peers. Other publicly traded super apps, including Tencent ($TCEHY), Alibaba ($BABA), Allegro ($ALEGF), NU Holdings ($NU), and MercadoLibre ($MELI), trade at significantly higher valuation multiples. Allegro is the closest to Kaspi in terms of peer size and user base. If Kaspi were to trade in line with peer valuation multiples, its stock price could have the potential to double. MercadoLibre and NU Holdings operate in South America, where, like Kaspi, they face elevated inflation and currency volatility. In particular, both companies are exposed to Argentina, a market characterized by hyperinflation and extreme currency devaluation, similar to the risks Kaspi encounters with the Kazakhstani tenge, yet they trade at much higher multiples.

Taking a combination of my valuations, I believe that a fair value for Kaspi is between $125 and $150. At its current price around $95.50, my fair value estimate gives the company a margin of safety between 23.6% and 36%.

Investment Thesis

Kaspi is well positioned to benefit from broader trends in mobile device adoption, cashless payments, and online shopping but the largest drivers of growth are coming from increased engagement on the Super App resulting in higher payment volumes, growing and increased penetration of business units, the growth of add on services such as advertising and delivery, and international expansion. Lower inflation and interest rates should also play favorably for Kaspi, as credit becomes more easily available and consumers regain confidence. I have no problem seeing continued growth rates between 15% and 20% over the next five years assuming international expansion gains traction.

Kaspi is a financially strong company with no debt and an investment-grade credit rating of Baa3 from Moody’s and BBB from Fitch. Management is highly customer-focused, prioritizing value creation and seamless user experience. The company’s deep integration into Kazakhstan’s economy and its Super App’s essential role in daily financial transactions provide a strong competitive moat, reinforcing confidence in its long-term sustainability and resilience.

My primary concern lies in the risk of ongoing geopolitical conflicts, which could lead to elevated inflation in Kazakhstan and the markets where Kaspi aims to expand. Persistent instability may weaken local currencies, drive up interest rates, and impact consumer spending, posing challenges to Kaspi’s growth and profitability. On one hand Inflation risk is a real but secondary concern for super app companies compared to the strength of their network effects and control over their financial ecosystem. While inflation can impact purchasing power, transaction volume, and financing costs, the dominant risk to these companies is often maintaining and growing their platform as the preferred medium of exchange within their markets. On the other hand, a significant depreciation of the tenge against the U.S. dollar could erode the USD-equivalent returns for ADR holders, even if Kaspi's underlying business performance remains strong.

At $95.50, Kaspi appears undervalued, presenting a compelling long-term investment opportunity. I have initiated a small position for observation and would consider increasing my stake if the price declines to around $80, provided geopolitical tensions remain stable and inflation does not accelerate. Moving forward, I plan to closely monitor Kazakhstan’s inflation and interest rate trends, regional geopolitical developments, and Kaspi’s overall performance in their international expansion and ability in increase customer penetration rates.

Thanks for reading! For updates on this company and more follow me on X.

Kaspi Revenue and Segemnt KPIs: Kaspi KPI Sheet